“반도체 공급부족 2023년에야 해소”

기사입력 2021.07.06 09:41

생산차질 2Q 정점 부품 재고 증가 하반기 완화

키움증권이 반도체 공급부족이 2분기 정점으로 재고가 증가하며, 하반기에는 완화되겠지만, 완전한 해소는 새로운 팹들이 늘어나는 2023년에야 이뤄질 것으로 전망했다.

키움증권 김지산 애널리스트는 1일 산업브리프를 통해 반도체 공급부족 이슈를 재점검했다.

이에 따르면 반도체 공급부족의 배경으로 코로나19로 인한 언택트 기기와 5G 스마트폰 수요 증가과정에서 PMIC를 중심으로 제품 MiX가 일치하지 않았고, 8인치 팹 투자 부족, 지정학적 불확실성과 같은 구조적 요인이 뒷받침되면서 공급부족이 발생했다.

특히 2분기 말레이시아 봉쇄, 대만의 물 부족 및 코로나 확산 등은 반도체 공급을 더욱 악화 시켰다.

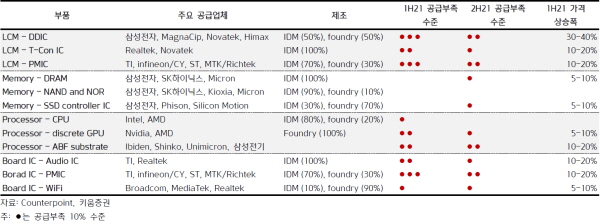

스마트폰은 전력반도체와 드라이버집적회로가 부족하고, 두 제품의 판가는 상반기에 20% 이상 상승했으며, 보급형 AP와 RFIC는 하반기에 수급 여건이 개선될 것으로 보인다.

중국와 인도 시장의 스마트폰 수요 약세와 재고 증가가 오히려 부품 수급을 안정화시키고 있는 것으로 나타났다.

노트북의 경우 재택근무와 원격교육의 장기화로 여전히 수요가 높으며, FC-BGA 기판의 공급부족이 두드러지며, GPU, 오디오IC, 와이파이 IC 등도 수급이 타이트하다.

하반기 언택트 가정용 수요가 둔화될 것이나, 컨택트 기업용 수요가 일부 상쇄 할 것으로 보인다.

인도 코로나 재확산과 봉쇄 영향으로서 2분기 스마트폰 수요는 대략 1,300만대 감소하고, 생산은 2,000만대 차질이 발생한 것으로 추정된다. 인도 내 생산능력은 삼성전자, Foxconn, Flextronics, Oppo 순으로 많다.

말레이시아 봉쇄는 NXP, TI, STM, Renesas 등 반도체 업체와 ASE, Inari 등 OSAT 업체들에게 차질을 초래했다.

대만 코로나 확산도 패키징, 테스트 공정 위주로 반도체 생산에 영향을 미쳤다.

TSMC 등 주요 파운드리 업체들은 올해 설비투자액을 50% 늘릴 계획이다. 이들은 기존 6인치 Fab 인수와 8인치 전환 등도 고려하고 있다. 2023년에 새로운 Fab들이 가동되면서 공급부족이 해소될 전망이다.

.jpg)

▲스마트폰 IC/칩 공급부족 상황(자료 : Counterpoint, 키움증권)

▲노트북 IC/칩 공급부족 상황(자료 : Counterpoint, 키움증권)

관련뉴스

-

.jpg)

[기획]스마트폰 하반기 전망-3Q 급반등·4Q 지속 ‘성장’

하반기 글로벌 스마트폰 시장은 반도체 공급부족완화, 코로나19 정상화, 피크 시즌 돌입 등에 힘입어 성장할 것으로 예상되며, 화웨이의 점유율 약화, LG전자의 스마트폰 철수에 따라 스마트폰 업체 간 시장 확대를 위한 치열한 경쟁이 펼쳐질 것으로 전망된다.

2021-06-15 오후 2:10:15by 배종인 기자

-

“2021년 반도체 성장률 24%로 상향”

IC인사이트는 반도체 공급부족, 가격 상승 등으로 2021년 전세계 IC 시장이 24% 성장할 것이며, 글로벌 IC 시장은 올해 처음으로 5,000억달러를 초과할 것으로 예상했다.

2021-06-18 오전 11:33:35by 배종인 기자

-

난국에 빠진 미국 반도체 공급망, 어디부터 손댈까?

미국 반도체 산업은 글로벌 반도체 시장 매출의 반을 차지하고 있다. 그러나 제조역량은 12%에 불과하다. 팬데믹과 몇 차례의 셧다운에 반도체 공급부족 사태를 겪은 美 백악관은 상무부를 통해 반도체 공급망 보고서를 작성했다. 보고서는 미국 중심의 반도체 공급망을 재건하기 위해서는 반도체 수요처 확대 및 전후방 산업에 대한 인센티브 확립이 중요하다고 밝혔다.

2021-06-28 오후 4:50:48by 이수민 기자

많이 본 뉴스

[열린보도원칙] 당 매체는 독자와 취재원 등 뉴스이용자의 권리 보장을 위해 반론이나 정정보도, 추후보도를 요청할 수 있는 창구를 열어두고 있음을 알려드립니다.

고충처리인 장은성 070-4699-5321 , news@e4ds.com