올해 웨이퍼 생산 8.7%↑...SK·TSMC 등 증설 영향

기사입력 2022.04.22 10:34

웨이퍼 생산능력 사상최고치 8.7%↑

투입량 증감은 -4.7~19% 넓은 편차

10개 신규 팹 증설 예정, 수요 견고

투입량 증감은 -4.7~19% 넓은 편차

10개 신규 팹 증설 예정, 수요 견고

반도체 수급난이 지속되고 있는 가운데 올해 전세계 반도체 업계에서 웨이퍼 생산능력이 증가한다는 전망이 나와 공급 부족을 해소할 수 있을지 관심이 모이고 있다.

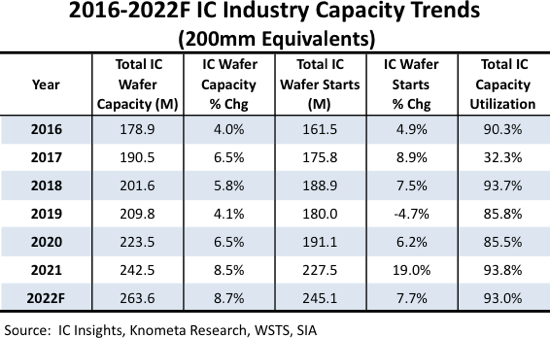

▲2016-2022년 반도체 산업 생산능력 추이 (200mm 상당 기준) *자료 - IC인사이츠

21일(현지시간) 반도체 시장조사기관 IC인사이츠에 따르면 8인치(200mm 상당) 기준 2022년 웨이퍼 생산능력은 사상최고치인 전년대비 8.7% 증가할 것으로 내다봤다. 반도체 수요 폭증에 힘입어 지난해 8.5% 증가율에 연이어 8%대 전망치를 예상했다. 더불어 10개의 신규 팹 증설이 성장에 영향을 미칠 것이란 관측이 나왔다.

IC인사이츠는 “IC산업의 변동성은 연간 웨이퍼 투입의 큰 변동에 영향을 받는다”며 반도체 업계에서 웨이퍼 생산능력의 증감은 시장 상황에 따라 변하지만 그것이 극적인 변동성을 보이진 않는다고 설명했다.

실제로 2016년부터 2021년까지 전년대비 웨이퍼 생산능력 증감률을 보면 4~8.5%의 범위를 보였지만 웨이퍼 투입의 증감률은 -4.7~19%까지 넓은 편차를 보여 더 큰 변동성을 나타냈다.

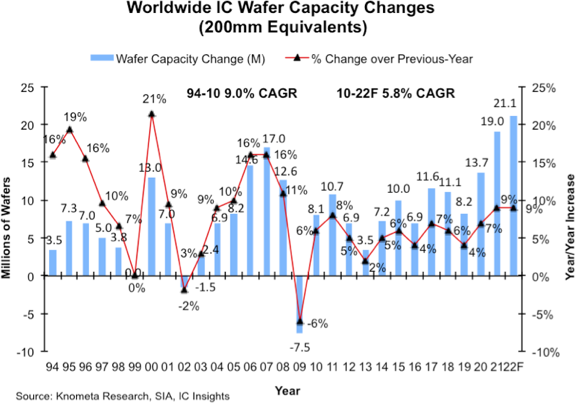

▲전세계 반도체 웨이퍼 생산능력 변화(200mm 상당 기준) *자료-IC인사이츠

전세계 웨이퍼 생산능력 변화를 보면 2002년 반도체 산업에서 처음으로 순손실이 발생했으며 2009년에 반도체 산업용량은 -6%의 기록적인 폭락세를 보이며 추락했다.

이는 2001년 닷컴버블에 의한 미증시 폭락과 2008년 서브프라임모기지사태에 의한 세계경기 둔화 직후에 반도체 업계에도 여파가 미쳐 설비투자 위축과 시장 침체가 발생했다. 더불어 2009년 8인치(200mm)이하 웨이퍼에서 다수의 팹들이 철수를 하며 반도체 시장이 일시적으로 시장 침체를 겪게 됐다.

2009년부터 2017년까지의 기간 동안 폐쇄되거나 용도 변경된 웨이퍼 팹은 총 92개에 달했으며, 이중 150mm가 41%, 200mm가 26%, 125mm이하에서 23%를 차지했다는 IC인사이츠의 조사결과가 있다.

IC인사이츠는 “2022년 반도체 산업 용량 예측에서 8.7% 증가는 10개의 새로운 12인치(300mm) 웨이퍼 팹의 추가로 인해 발생할 것”이라고 밝혔다. 이는 SK하이닉스와 윈본드의 대규모 신규 메모리 팹과 TSMC의 대만 및 중국에 증설될 3개의 신규 팹에서 가장 큰 케파 증가가 예상된다고 설명했다.

이밖에 전력 디스크리트 및 센서를 생산하는 실란(Silan)의 팹, 아날로그 장치 생산에 텍사스 인스트루먼트(TI)의 RFab2 시설, 혼합 신호·전력·RF 및 파운드리를 위한 ST와 Tower의 팹, 파운드리 부문에 SMIC의 신규 팹과 함께 전력반도체용 CR 마이크로 팹을 포함한다.

IC인사이츠는 “인플레이션 압력과 지속적인 공급망 문제가 있음에도 반도체 수요는 여전히 견고하다”며 “올해 반도체 단위 출하량은 9.2% 증가할 것으로 예측한다”고 밝혔다.

더불어 “10개의 새로운 웨이퍼 팹이 가동을 시작하더라도 견고한 수요는 2022년 전세계 설비 가동률을 93%까지 끌어올려 높은 수준을 유지할 것”이라고 전망했다.

관련뉴스

-

8인치 반도체, 높아지는 위상...호실적에 설비투자 확대

코로나19 이후 반도체 수요가 급증하며 8인치(200mm) 파운드리의 몸값이 점점 높아지고 있다. 이에 관련 업계에서 생산라인을 풀가동해 생산량을 늘리고 있으며 설비투자에도 적극적인 움직임을 보이고 있다.

2022-04-13 오전 10:09:00by 권신혁 기자

-

반도체 출하량 9.2% 증가 전망...사상 최고 4,277억 유닛

전세계적으로 반도체 수요가 급증함에 따라 전세계 반도체 출하량에서 올해 9.2% 증가를 예상했으며, 향후 5년간 7~8% 성장률을 기록할 것이라 예측했다.

2022-04-14 오전 10:54:44by 권신혁 기자

-

글로벌 반도체 장비 매출액 지난해 44% 증가

반도체 수요 급증으로 생산라인이 풀가동되고 있는 가운데 각 나라별 반도체 기업들이 생산설비에 공격적인 투자에 나서며 전세계 반도체 장비 매출액이 크게 증가하고 있다.

2022-04-15 오전 10:21:12by 권신혁 기자

많이 본 뉴스

[열린보도원칙] 당 매체는 독자와 취재원 등 뉴스이용자의 권리 보장을 위해 반론이나 정정보도, 추후보도를 요청할 수 있는 창구를 열어두고 있음을 알려드립니다.

고충처리인 장은성 070-4699-5321 , news@e4ds.com