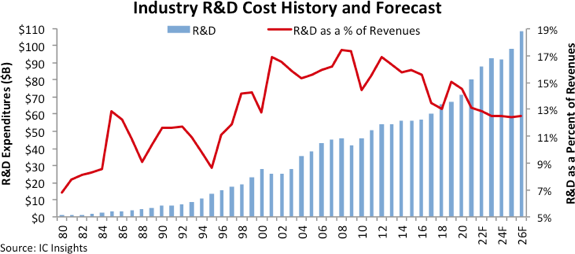

▲반도체 산업 R&D 비용 추이(그래프-IC인사이츠)

R&D 비용(좌), 매출 대비 R&D 비율(우)전세계 반도체기업 R&D 지난해比 18%↑

26년까지 1,086억달러 확대, CAGR 5.5%

전세계 반도체 개발 경쟁이 치열해짐에 따라 연구개발비에 쏟아붓는 금액이 지난 40년간 꾸준히 증가했다. 2026년 1,100억달러까지 확대될 것으로 전망되는 가운데 인텔이 사상 최대 R&D 지출을 감행했으며 삼성이 2위로 그 뒤를 바짝 추격하고 있다.

최근 5일(현지시간) IC인사이츠가 발표한 보고서에 따르면 전세계 반도체 기업들의 연구개발(R&D) 지출에서 상위 10개사가 지난해 대비 18% 지출액을 늘렸으며 21개사가 연구개발에 10억달러 이상을 투자했다고 밝혔다.

IC인사이츠는 전세계 반도체 기업들의 R&D 지출은 지난해 714억달러로 13% 이상 상승한 금액을 기록했으며 2022년 805억달러로 9% 증가할 것으로 전망했다. 반도체 기업의 총 연구개발 지출은 2026년까지 연평균성장률(CAGR)에 있어서 5.5% 증가한 1,086억달러를 기록할 것으로 추정했다.

IC인사이츠는 인텔이 2021년 R&D 지출에서 다른 모든 반도체 공급업체들을 제치고 업계 전체 약 19%를 차지했다고도 밝혔다. 인텔은 차세대 IC 프로세싱 기술을 출시하고, 첨단 웨이퍼 파운드리 서비스의 주요 공급업체로 자리매김하기 위해 집중하고 있다고 설명했다. 이를 위해 2021년 R&D 지출에서 지난해 대비 12% 증가한 사상 최대 금액인 152억달러를 기록했으며, 2019년과 2020년의 R&D 지출 차이는 변동폭이 크지 않은 것으로 나타났다.

삼성은 IC인사이츠의 2021년 R&D 순위에서 2위를 차지했으며 2020년 23% 증가에 이어 지난해 13% 증가한 65억달러로 R&D 지출이 추정된다고 언급했다. 또한 국내 메모리 대기업은 파운드리 시장 강자인 TSMC와 경쟁하기 위해 5나노(nm) 첨단 로직 프로세스에 집중해 R&D 지출을 가속화하고 있다고 덧붙였다. 2020년 26% 증가에 이어 2021년 R&D 지출을 약 45억 달러로 늘렸다.

IC인사이츠의 2021년 R&D 순위는 21개 반도체 공급업체가 R&D에 10억달러 이상 지출한 것으로 나타났다. R&D 순위에서 상위 10개사는 지난해 업계 R&D 총액의 약 65%에 해당하는 526억달러로 직전 해 대비 18% 늘어난 것으로 조사됐다.

상위 10개사의 매출 대비 R&D 비율은 2020년 14.5%와 비교해 지난해는 13.5%를 기록해 직전 해 대비 다소 떨어진 수치를 보였다.

2020년 전세계가 코로나19 바이러스로 인해 위기를 겪었을 때, 반도체 공급업체들은 치명적인 팬데믹을 늦추기 위한 공장 폐쇄 및 기타 긴급조치를 단행했음에도 반도체 산업 매출은 11% 이상 성장했다. 반면 R&D 지출 부문에서는 증가를 억제하는 경향을 보였다.

전세계 반도체 산업 매출에서 반도체 R&D 지출이 차지하는 비율은 2019년 15.1%에서 2020년 14.5%, 2021년 13.1%로까지 떨어졌다. 지난 40년간 반도체 R&D 지출 수준은 지속적으로 증가한 반면 업계의 매출 대비 R&D 비율은 증감이 수시로 변화하는 모습을 보였다.

이는 글로벌 경기와 밀접한 관련이 있는데 전체 반도체 R&D 지출은 역사적으로 4번의 하락시장을 경험했다. 닷컴버블 붕괴와 함께 지속된 경기침체로 2001년 10%와 2002년 1%의 감소세, 서브프라임 모기지 사태로 인한 금융붕괴로 글로벌 경기 침체가 발생해 산업이 타격을 받은 2009년 10%, 경기침체기인 2019년 1% 하락세를 기록했다.

2008년과 2009년 글로벌 경기 침체 여파로부터 반도체 R&D지출은 지난 몇 년간 크게 회복했지만 이후 지속적인 경제적 불확실성과 인수합병의 물결을 포함해 다양한 요인들로 인해 지난 10년간은 지출이 둔화됐다고 보고서는 평가했다.

2000년 이후 전세계 반도체 매출에서 차지하는 총 반도체 R&D 지출 비용은 5번(△2000년 △2010년 △2017년 △2018년 △2020년)을 제외하면 모든 기간 동안 평균 14.5%를 초과했다. 평균 이하의 5년은 반도체 공급업체의 R&D 지출 감소가 발생했다기보다는 전체 반도체 매출이 성장했다는 점과 더욱 관련이 있다고 보고서는 부연했다.

.jpg)