국내 반도체 소자·소재·설계·장비별 실적 분석

반도체 229개 기업, 전년대비 23% 매출 성장

e4ds news가 국내 반도체 관련 기업 229개사를 대상으로 2021년 경영실적을 조사했다. 반도체 229사 총 매출액은 352조3,221억원에 달했으며 2020년 대비 23% 증가해 연평균 16%의 높은 성장률을 기록했다.

지난해 높은 실적 증가는 반도체 수요 폭발로 인한 판매량 증가와 가동률 증가로 인한 소재 사용량 증가에 기인한다. 또한 대규모 투자로 인한 장비 투입량 증가로 반도체 산업 전체가 성장을 이룩했다. 2022년에도 지난해에 이어 높은 수요증가와 천문학적 투자로 인해 국내 반도체 산업이 성장할 것으로 전망된다.

■반도체 소자, 삼성·SK하이닉스로 국내시장 대표

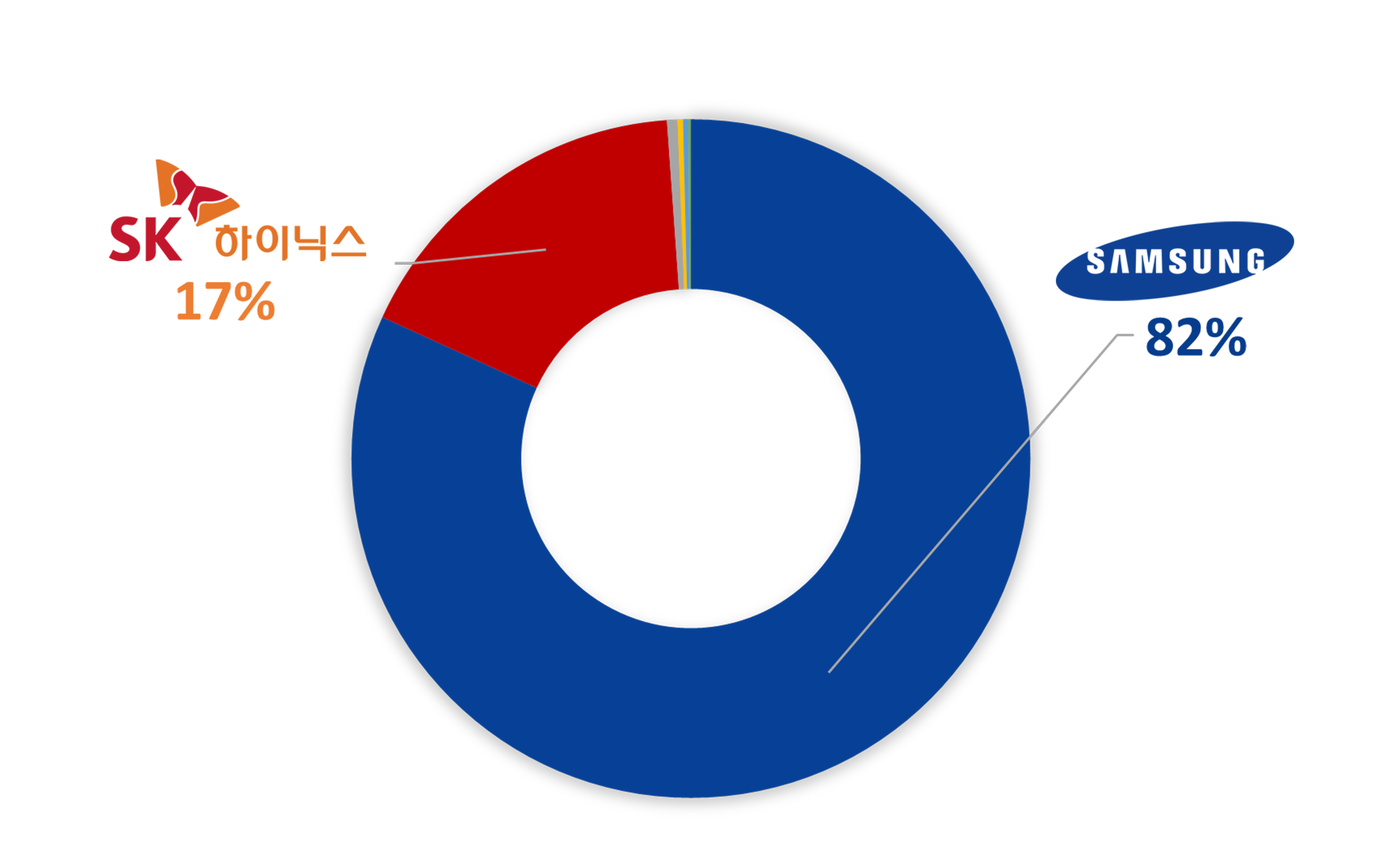

▲2021년 반도체 소자 업체 매출 비중

국내 반도체 소자 7사의 매출은 244조582억원으로 전년대비 23% 증가한 실적을 보였다. 반도체 소자부문은 국내 반도체 매출의 64%를 차지할 정도로 비중이 높으며, 그 중 삼성전자가 82%를 차지해 소자업계를 대표한다고 할 수 있다.

삼성전자는 지난 2021년 199조7,447억원의 매출을 기록해 전년대비 20% 증가했으며 이중 가전, 기타 사업을 제외한 반도체 매출이 125조9천억원에 달했다. 전반적인 공급 확대로 인해 사상 최고의 실적을 경신했으며, 이에 따라 첨단 공정 확대 및 대규모 투자로 국내 반도체 산업 전반을 이끌고 있다.

SK하이닉스는 41조5,573억원의 매출을 기록해 전년대비 36% 매출 증가를 기록하며, 사상최대의 매출 실적을 달성했다. SK하이닉스는 D램 사업에서 PC, 서버향 제품 등 수요 증가에 적극 대응했고, 낸드 사업에서도 128단 경쟁력을 바탕으로 시장 평균을 뛰어넘는 판매량 증가율을 기록한 바 있습니다.

■반도체 소재, 작은 공급난에도 큰 영향력

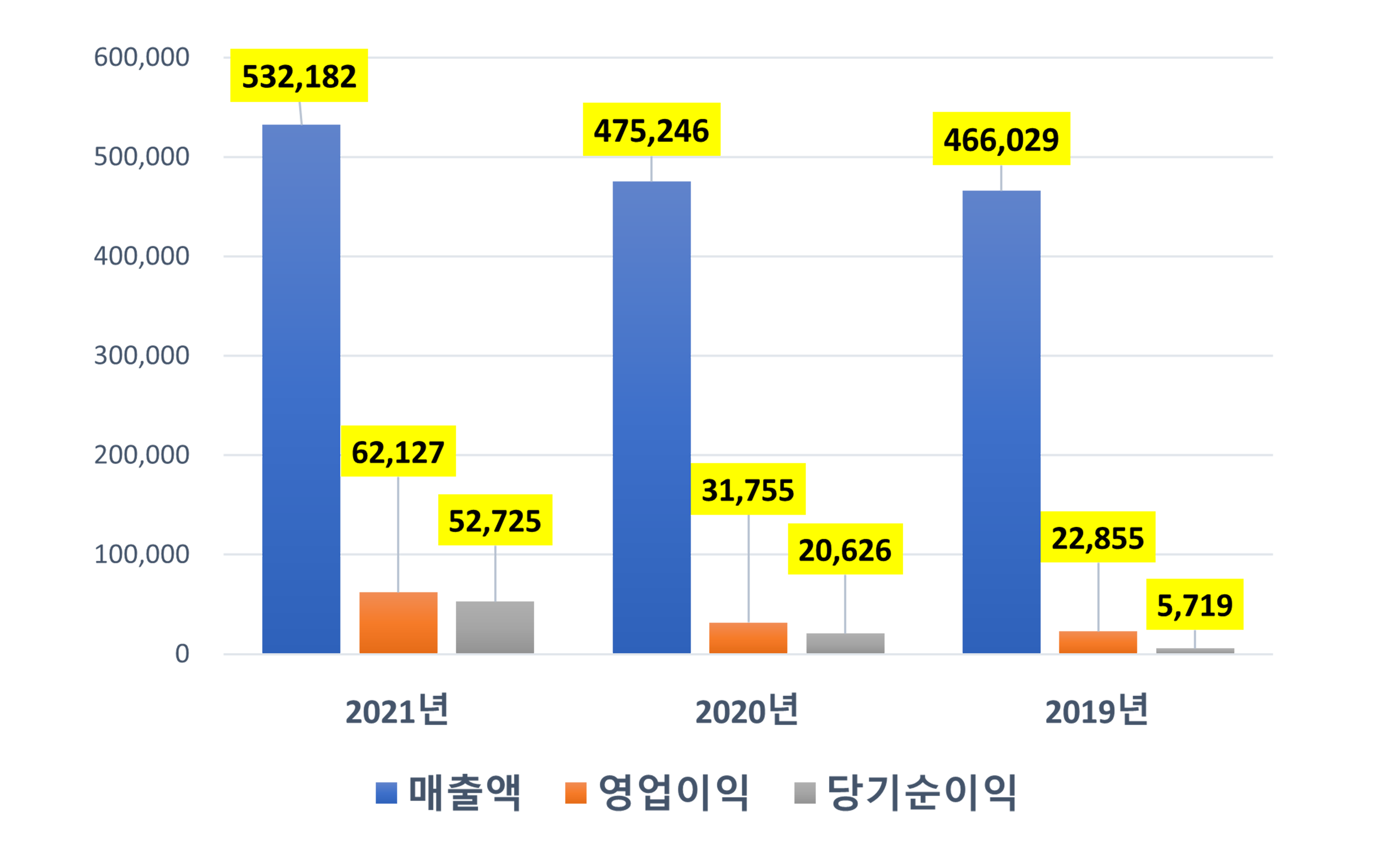

▲반도체 소재 51개사 경영실적 종합

반도체 소재에는 감광제, 실리콘카바이드, 전구체, 연마체, 고순도 특수가스, 세정제 등 수천가지의 다양한 소재들이 존재한다.

지난 2019년 일본의 수출 규제로 인해 대국민적 관심사로 주목받았는데, 당시 사건에서도 알 수 있듯이 아주 적은 물량의 소재 공급이 중단돼도 반도체 생산공정에 문제가 발생해 반도체 전공정에 미치는 영향이 크다.

특히 반도체 소재의 경우 기술력의 차이로 인해 해외 수입에 의존하는 경우가 큰데 일본 수출 규제 당시 주목됐던 3개 품목의 경우 플루오린 폴리이미드는 일본이 세계 시장 90%를 점유하고 있다. 포토레지스트의 경우 일본이 세계시장 90%를 점유하고, 우리나라의 경우 일본산의 수입비중이 91.9%에 달한 것으로 조사됐다. 또한 불화수소의 경우 일본이 세계시장 70%를 점유하고 있고, 우리나라의 경우 일본산의 수입비중이 95%에 달했다.

해당 사건 이후 우리나라는 매년 반도체 소재에 1조원 이상을 투자하고 있으며, 반도체 국산화를 위해 많은 노력을 하고 있지만 상당한 시간이 필요할 것으로 전망된다.

이러한 반도체 소재 51社의 2021년 매출은 53조2,182억원을 기록해 전년대비 12% 증가했고, 최근 연평균 7%의 성장을 지속하고 있다. 영업이익은 6조2,127억원을 기록해 전년대비 96% 증가했고, 당기순이익은 5조2,725억원을 기록해 전년대비 156% 증가했다.

업체별로는 LG화학이 20조4,710억원을 기록하며 1위를 차지했으며 이어 삼성SDI가 11조5,818억원으로 2위에 이름을 올렸다. 그 뒤로 케이씨씨 2조2,866억원, 효성화학 2조1,089억원, SK실트론 1조8,265억원을 기록하며 상위권을 차지했다.

반도체 소재는 반도체 가동률 증가 및 초미세화 추세 속에 다양한 공정이 추가되며, 사용량이 지속 증가하고 있다. 2022년에도 반도체 소재 시장은 반도체 수요 증가에 비례해 지속 상승할 것으로 전망된다.

다만 GWP 등 ESG와 관련된 문제가 대두되며, 향후 새로운 소재 발굴이 해결과제로 부상하고 있다.

■반도체 설계, 공급난 타격에도 드러나는 포텐셜

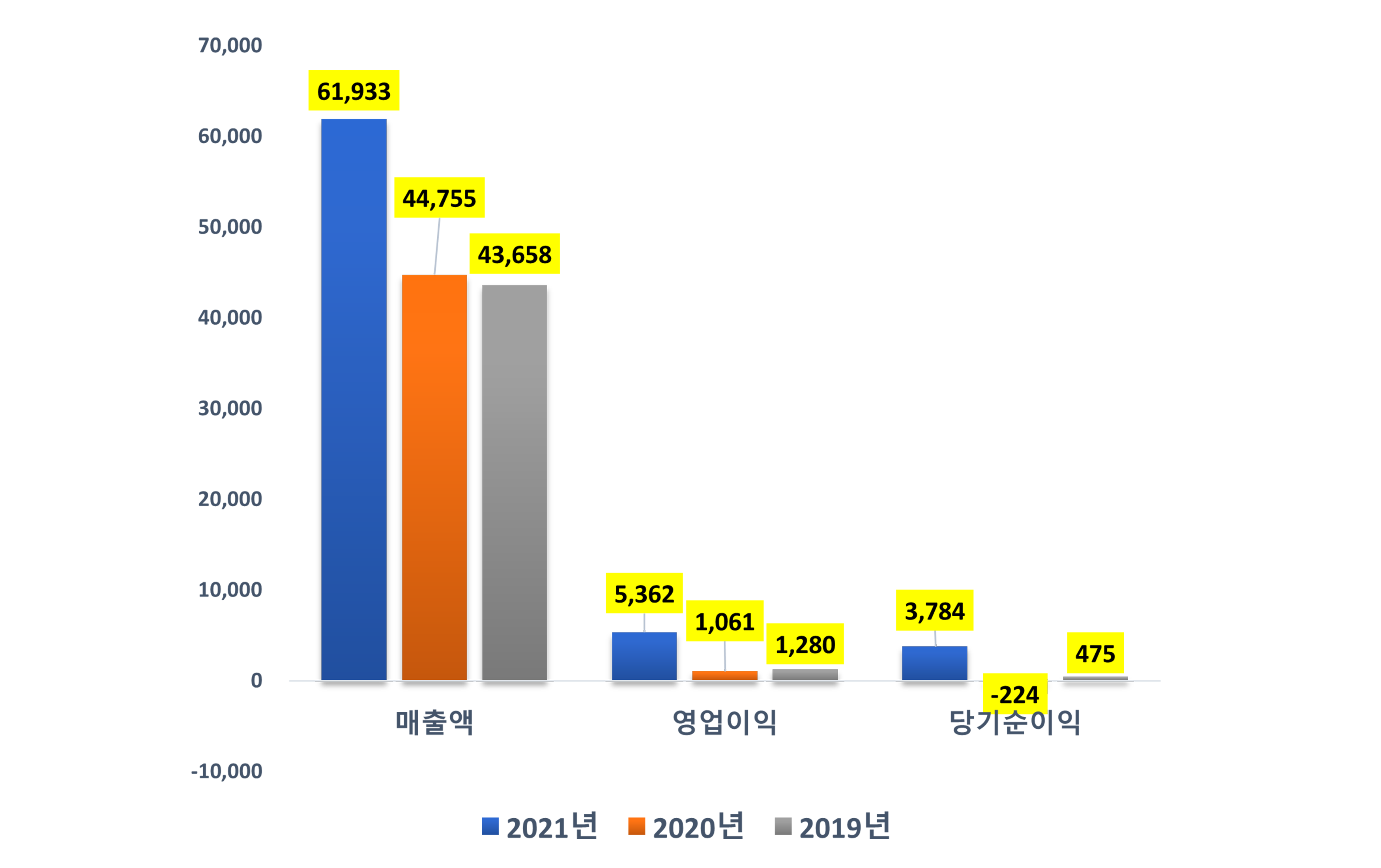

▲반도체 설계 40개사 경영실적 종합

반도체 설계 전문 기업인 팹리스(fabless)는 지난해 반도체 수급난이 발생하며, 주목받기 시작했다.지난해 자동차용 반도체를 비롯해 전력반도체 등 부품으로 사용하는 시스템 반도체 대부분이 공급난을 겪었고, 현재도 문제 해결이 요원한 상태이다.

이런 시스템 반도체들은 팹을 가지고 전문적으로 생산하는 글로벌 기업도 있지만, 거의 대부분이 파운드리를 이용해 설계한 제품을 위탁 생산하는 경우가 많다. 이에 지난해 파운드리 확보를 하지 못했던 팹리스의 경우 제품 생산에 차질을 빚으며, 어려움을 겪기도 했다.

반면 반도체 부족 속에 제품 생산에 성공한 기업들의 경우 실적 상승 및 영업이익 개선의 고성장을 기록했다.

반도체 설계 40개사의 2021년 경영실적을 살펴보면 매출이 6조1,933억원으로 전년대비 38% 증가했고, 영업이익은 5,362억원으로 전년대비 405%의 경이로운 성장을 보여줬다. 당기순이익도 3,784억원으로 흑자전환에 성공했다.

2022년 현재 반도체 부품난이 지속되고 있고, 납기 또한 1년 이상 밀려있는 것으로 전해지고 있지만 파운드리 확보만 가능하다면 팹리스들의 지속적인 성장이 기대되는 상황이다.

LX세미콘이 1조8,988억원을 기록하며 설계부문 매출 1위를 차지했으며 이어 현대오토에버 1조6,850억원, 한국아이비엠 5,582억원, 실리콘마이터스 3,294억원 등을 기록하며 매출 상위권에 이름을 올렸다.

■반도체 장비, 소자 업체의 설비 투자 증가 영향

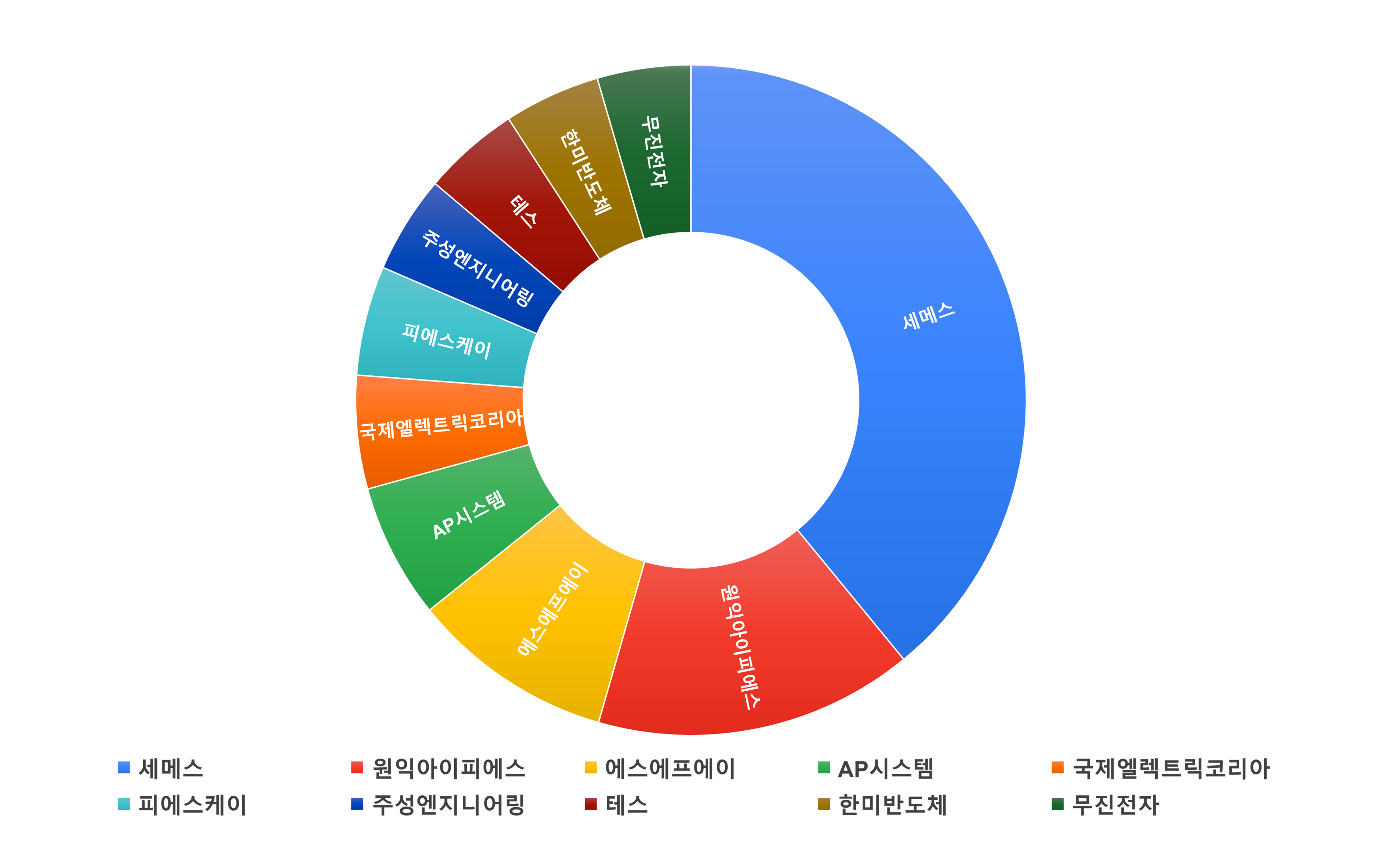

▲2021년 반도체 장비 상위 10개사 매출 순위(12시 기준 시계 방향으로 점유율 높은 순)

반도체 장비는 웨이퍼 제조, 산화공정, 포토공정 등 반도체 8대에 쓰이는 장비를 이야기하며, 다양한 공정 장비들이 존재한다.

국내 반도체 장비 77社의 2021년 매출은 16조8,943억원을 기록해 전년대비 23% 증가했다. 영업이익은 2조1,746억원으로 전년대비 37% 증가했고, 당기순이익은 1조9,009억원으로 전년대비 56%증가에 달했다.

이와 같은 실적 증가는 2021년 국내 반도체 소자 업체들의 대규모 투자가 진행됐기 때문으로 분석된다. 국내 반도체 장비사들의 매출은 소자 업체들의 투자에 달렸다고 할 수 있으며, 최근 가장 큰 투자는 삼성전자 평택 공장 투자와 관련돼 있다고 해도 과언이 아니다.

국내 반도체 장비 매출 1위는 세메스로 3조1,281억원의 매출을 기록해 전년대비 42%의 높은 매출 증가세를 기록했다. 주요 매출처는 삼성전자로 2022년 9월까지 3조5,991억원의 수주총액을 기록하고 있고, 수주잔고도 4,710억원에 달해 2022년에도 꾸준한 성장이 기대된다. 2위로는 약 1조2,000억원을 기록한 원익IPS, 이어 3위는 SFA가 약 7,800억원을 기록했다.

.jpg)

.jpg)

.jpg)