12인치 팹 투자 규모 증가일로 탔다 "증가액 대부분 메모리에 집중돼"

기사입력 2020.11.05 12:51

코로나19 팬데믹에 세계적인 디지털화 가속

반도체 수요 급증하며 팹 투자 규모도 증가

12인치 팹 투자 규모, 2023년에 최고치 전망

올해 팹 투자 규모가 코로나19 팬데믹으로 인한 세계적인 디지털화 가속으로 인해 급증할 것이며, 이 추세가 2021년까지 지속될 것이란 전망이 나왔다.

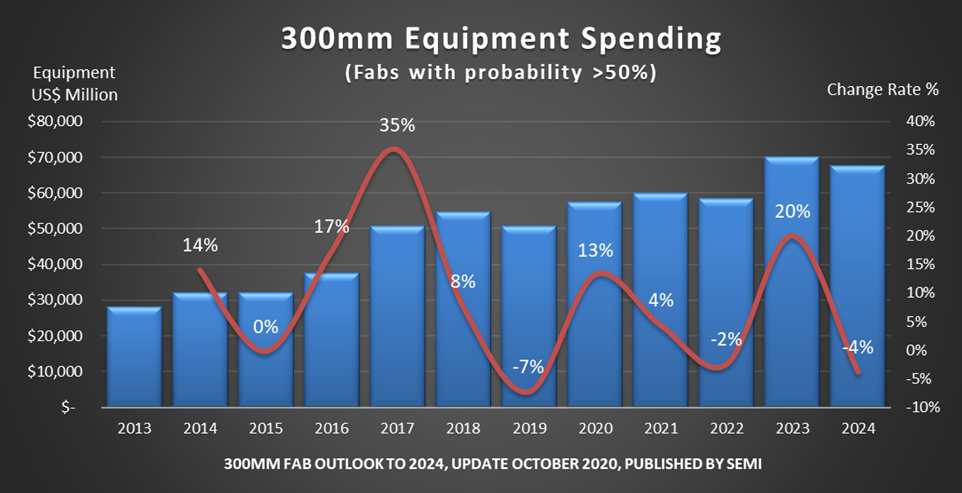

국제반도체장비재료협회(SEMI)가 5일 발표한 ‘300mm 팹 전망 보고서’에 따르면 300mm(12인치) 팹 투자 규모는 올해에 2019년 대비 13% 증가하여 2018년의 기존 최고치를 경신하고, 2023년에는 20%까지 증가할 것으로 보인다.

▲ 300mm 팹 투자 규모 증감 추이 [그래프=SEMI]

코로나19 외에도 클라우드 서비스, 서버, PC, 게임 및 헬스케어 기술 등의 수요 증가로 인해 팹 투자액은 지속해서 성장할 것으로 전망된다. 특히 5G, AI, IoT, 자율주행, 머신러닝 등의 기술 발전으로 대규모 데이터가 증가하며, 이 데이터를 처리하고 저장하는 반도체 분야의 투자를 촉진하고 있다.

반도체 팹 투자는 2021년까지 지속해서 성장할 것으로 보인다. 특히 올해는 전년 대비 13% 성장할 것으로 보이며 2021년에는 4%의 성장세가 예상된다. 2022년에는 2% 소폭 하락할 것으로 보이지만 2023년에는 20% 증가한 약 700억 달러를 기록하며 역대 최대 규모의 팹 투자가 예상된다.

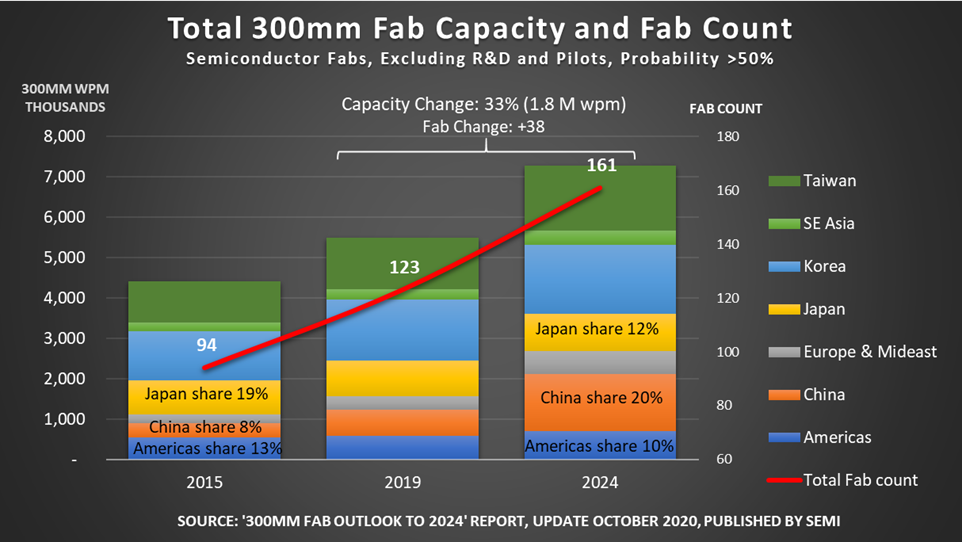

SEMI의 300mm 팹 전망 보고서는 올해부터 2024년까지 최소 34개의 신규 300mm 팹이 건설될 것으로 예상했다. 이 기간에 월간 팹 생산량에 대해서 약 180만 달러가 투자되어 월 웨이퍼 생산량은 2024년 700만 장을 넘어설 것으로 보인다.

신규 팹 중 11개는 대만, 8개는 중국에서 건설되며, 이는 전체 신규 팹의 절반을 차지하는 수치이다. 2024년까지 300mm 팹은 전 세계적으로 161개가 될 것으로 보인다.

▲ 지역별 300mm 팹 증가 추이 [그래프=SEMI]

중국은 300mm 팹 생산량의 점유율을 빠르게 늘려가는 지역으로, 2015년 8%에서 2024년에는 20%(월 생산량 150만 장)까지 점유율을 가져갈 것으로 보인다.

중국 국적이 아닌 기업들이 이러한 성장을 이끌 것이나, 중국 국영 반도체 기업들도 생산량 투자를 가속화하고 있다. 중국 국영 반도체 기업들의 자국 내 팹 생산량은 올해 약 43%에서 2022년에는 50%, 2024년에는 60%에 이를 전망이다.

300mm 웨이퍼 생산량에 있어 일본의 점유율은 2015년 19%에서 2024년 12%로 계속 하락 추세를 그릴 전망이다. 북미 지역의 점유율도 2015년 13%에서 2024년 10%로 떨어질 것으로 보인다.

우리나라는 300mm 팹 분야 투자가 가장 많이 이뤄지는 지역으로, 올해부터 2024년 사이에 약 150~190억 달러가 투입될 전망이다. 뒤이어 대만이 약 140~170억 달러, 중국이 110~130억 달러를 투자할 것으로 보인다.

팹 투자 규모가 다소 작았던 지역들의 올해와 2024년 사이의 투자액은 가파르게 증가할 것으로 예상된다. 유럽 및 중동 지역은 164% 증가할 것이며 동남아시아 지역은 59%, 북미는 35% 그리고 일본은 20%가 증가할 것으로 보인다.

◇ 팹 투자, 메모리 및 파워 반도체에 집중

300mm 팹 투자액 증가의 대부분은 메모리 분야가 차지할 것으로 보인다. 300mm 메모리 팹에 대한 투자는 올해부터 2023년까지 매년 한 자릿수 후반대 성장이 예상되며 2024년에는 약 10%의 성장이 전망된다.

D램 및 3D 낸드 분야에 대한 300mm 팹 투자액은 매년 다른 추이를 보일 것으로 전망되지만, 로직 및 MPU 분야에 대한 투자는 올해부터 2023년까지 꾸준한 성장이 예상된다.

전력 반도체에 대한 투자는 2021년에 약 200% 성장이 예상되며 2022년과 2023년에는 두 자릿수 성장세를 이룰 것으로 보인다.

이수민 기자

관련뉴스

-

메모리·이미지·파워 반도체 장비 투자 급증 조짐 보여

SEMI의 세계 팹 전망 보고서에 따르면, 2021년 반도체 팹 장비 투자액은 2020년 대비 약 24% 증가한 677억 달러에 이를 전망이다. 메모리 팹이 300억 달러 규모로 가장 큰 투자를 할 것으로 보이며, 로직 팹 및 파운드리가 290억 달러로 그 뒤를 이을 것으로 보인다.

2020-06-10 오후 1:01:50by 강정규 기자

-

2020년 팹 장비 투자액, 메모리 분야에서 가장 높을 전망

SEMI가 최신 팹 전망 보고서를 내고 전 세계 전처리 공정 팹 장비 투자액이 올해에 8%, 내년에 13% 증가할 것으로 전망했다. 메모리 분야의 올해 팹 장비 투자액은 264억 달러를 기록할 것으로 보이며, 파운드리 분야는 232억 달러를 달성할 것으로 보인다.

2020-09-09 오후 2:41:57by 이수민 기자

-

SK하이닉스, 인텔 '낸드' 품는다 "D램 편중구조 탈피"

SK하이닉스가 인텔의 낸드 메모리 및 스토리지 사업을 인수한다. 인수 대상은 인텔의 낸드 SSD, 낸드 단품과 웨이퍼 비즈니스, 중국 다롄 팹 등이며, 인수 총액은 90억 달러, 우리 돈으로 약 10조3천억 원이다. 인수 대상에 옵테인 사업은 포함되지 않는다.

2020-10-20 오후 12:25:31by 이수민 기자

많이 본 뉴스

[열린보도원칙] 당 매체는 독자와 취재원 등 뉴스이용자의 권리 보장을 위해 반론이나 정정보도, 추후보도를 요청할 수 있는 창구를 열어두고 있음을 알려드립니다.

고충처리인 장은성 070-4699-5321 , news@e4ds.com