빠르게 성장하고 있는 자동차용 디스플레이 시장에서 우리나라 기업들이 살아남기 위해서는 기존에 선점하고 있는 OLED 시장에서 주도권을 지켜내야 생존 할 수 있을 것으로 분석됐다.

.jpg)

▲현대차 아이오닉6 디스플레이(사진 : e4ds news)

LCD 중·대만 선점, OLED 2027년 17.2%까지 비중 커져

시장 수요변화 프리미엄 라인·대형 중심 OLED 채용확대

빠르게 성장하고 있는 자동차용 디스플레이 시장에서 우리나라 기업들이 살아남기 위해서는 기존에 선점하고 있는 OLED 시장에서 주도권을 지켜내야 생존 할 수 있을 것으로 분석됐다.

한국디스플레이산업협회는 차량용 디스플레이 밸류체인, 글로벌 경쟁력 분석 데이터를 담은 ‘차량용 디스플레이 밸류체인 분석 리포트’를 지난 2일 발표했다.

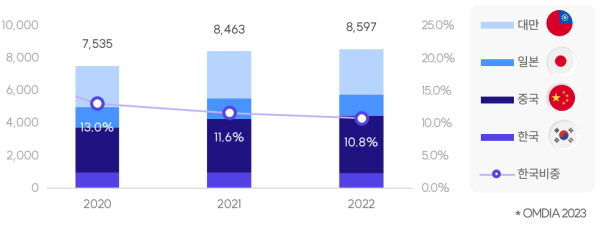

이에 따르면 2022년 기준 차량용 LCD는 86억달러로 거대 내수시장을 바탕으로 빠르게 점유율을 확대한 중국이 38.4%, 일찍이 차량용 디스플레이 시장에 참여한 대만이 33.7%, LCD 생산을 지속 감소 중에 있는 일본과 한국은 각각 14.8%, 13.1%으로 동북아 4개국이 차량용 LCD 생산에 모두 참여하는 것으로 나타났다.

▲차량용 디스플레이 LCD 국가별 규모(백만불)

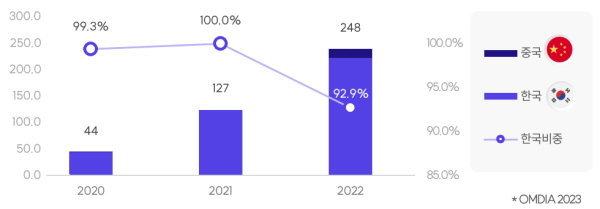

반면에 OLED는 2022년 기준 전체 2억5,000만달러 시장에서 한국이 2억3,000만달러로 약 93%, 중국은 2,000만달러로 약 7%의 비중을 차지하며 한·중 양국만이 경쟁 중에 있는데 한국은 차량용 OLED에서 압도적으로 우위를 점하고 있는 것으로 나타났다.

▲차량용 디스플레이 OLED 국가별 규모(백만불)

다만 OLED 투자 확대로 시장 침투율을 높이고 있는 중국은 2021년 0%에서 2022년 7.1%로 점유율을 확대하고 있어서 향후 차량용 OLED 시장에서도 경쟁 심화 양상이 나타날지 주목해 볼 필요가 있다.

지난 5년(2017∼2022년)간 LCD 및 중소형 사이즈에 집중됐던 차량용 디스플레이 시장은 연평균성장률(CAGR)이 약 4.7%인 반면에 앞으로 대형화 추세에 따라 이 시장은 2027년에는 126억불까지 연평균 약 7.8% 성장할 것으로 전망하고 있다.

기술별로 보면 차량용 LCD는 2022년에 약 97.2%의 점유율을 차지했으나 대형 및 고화질 디스플레이 수요 증가에 따라 감소 추세에 있으며, OLED는 2022년 2.8%에서 2027년 17.2%까지 비중이 점차 커질 것으로 예상된다.

2023년 현재까지 출시된 자동차 중 가장 높은 자율주행 수준인 조건부 운전자동화(레벨3) 기능이 탑재되면서 차량 내부 공간의 활용성 변화로 자동차 업계의 디스플레이 요구사항도 달라지고 있다.

특히 자동차 업계는 운전 시 햇빛 반사를 뛰어넘는 밝기 수준(500∼1,000nits)과 극한의 온도변화(-30∼70℃)에도 작동에 영향이 없으면서 자유로운 디자인 변형과 고화질 구현에도 영향이 없는 디스플레이를 요구하고 있다.

이러한 요구조건을 부응하는 디스플레이는 현재 OLED가 가장 적합함에 따라 완성차 업계는 프리미엄 라인 중심으로 OLED 채용을 확대하고 있다.

차량용 디스플레이의 종류별로 보면 OLED는 엔터테인먼트를 활용하는 분야에 집중되고 있다. 매출액 기준 Center Stack Display의 OLED 비중은 2020년 0.6% 수준에 불과한 반면에 2023년 8.0%로 성장, 차량 내 동승자가 이용하는 Passenger Display는 2023년 46.3%의 비중을 차지하는 것으로 나타났다.

또한 자동차 업계가 주행정보 뿐 아니라 영화 등 컨텐츠를 하나의 화면에 담으려는 수요증가로 차량용 디스플레이는 점차 대형화 될 수밖에 없다. 이는 디스플레이 업계 입장에서 디스플레이 대형화는 곧 수익성 확보로 연결되어 차량용 디스플레이 시장성 확대에도 긍정적인 요인으로 작용할 것으로 전망한다.

Center Stack Display와 Cluster의 경우 주행정보와 각종 볼거리, 차량의 상태 정보 등 정보 전달과 엔터테인먼트 기능의 강화로 10인치 이상의 패널이 전년대비 각각 13.3%, 17.2%로 빠르게 증가하고 있다.

이러한 대형화 추세와 함께 국내 디스플레이 제조기업 LGD·삼성D는 Hybrid OLED 패널제조, 투 스택 탠덤(Tandem) 기술을 통해 OLED의 짧은 수명이라는 한계를 극복했다. 이러한 기술개선은 OLED 적용확대를 앞당기고 높은 이윤 확보까지 기대할 수 있게 됐다.

한국디스플레이산업협회 이동욱 부회장은 “세계 자동차 업계는 차별화 요소를 전장부품으로 확장시키고 있고, 전장부품에서 디스플레이 기술이 차지하는 중요도가 점점 높은 주목을 받고 있는 상황”이라고 밝혔다.

또한 “지난해 반도체 공급부족으로 자동차 생산 지연 문제를 겪은 것처럼, 앞으로 OLED 등 프리미엄 디스플레이의 안정적인 공급측면에서 자동차-디스플레이 산업 간 협력 확대는 선택이 아닌 필수”라며 “급격히 부상하는 차량용 디스플레이의 수출 및 투자 지원을 위한 안정적인 공급망 생태계 전략 마련이 무엇보다 필요하다”고 밝혔다.

.jpg)