우리나라의 비메모리 반도체의 세계 시장점유율이 일본의 1/3, 중국의 1/2인 3.3%에 불과하고, 그 마저도 삼성전자, LX세미콘, SK하이닉스 3사에 집중돼 있어 냉철하고 다각적인 역량 진단에 기반한 국가적 시스템반도체 전략 마련이 시급한 것으로 나타났다.

20조원 규모 6위, 삼성·LX·SK 비중 90%

다종 소자·기술 포괄 포트폴리오 접근 必

우리나라의 비메모리 반도체의 세계 시장점유율이 일본의 1/3, 중국의 1/2인 3.3%에 불과하고, 그 마저도 삼성전자, LX세미콘, SK하이닉스 3사에 집중돼 있어 냉철하고 다각적인 역량 진단에 기반한 국가적 시스템반도체 전략 마련이 시급한 것으로 나타났다.

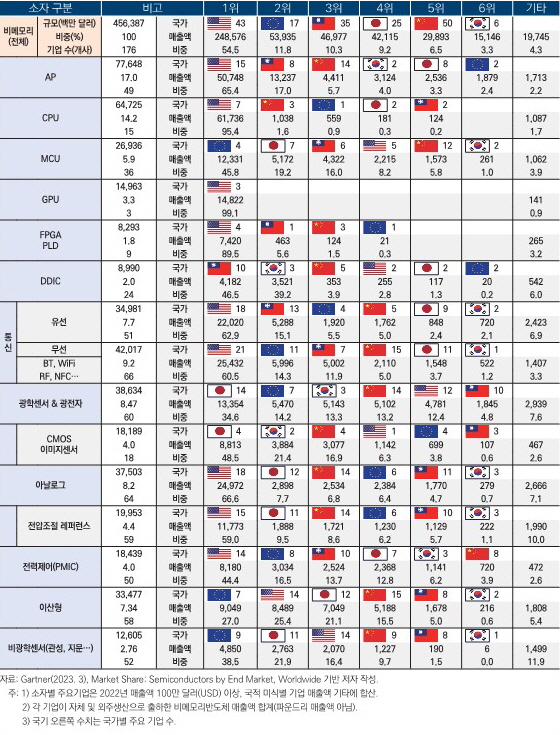

산업연구원(KIET, 원장 주현)이 최근 발표한 ‘세계 비메모리 반도체 시장 지형과 정책적 시사점’ 보고서에 따르면 2022년도 세계 비메모리 반도체 시장 규모는 총 593조원으로, 국가별 점유율은 미국이 압도적 1위(323조원, 54.5%)를 차지한 가운데, 유럽 2위(70조원, 11.8%), 대만 3위(61조원, 10.3%), 일본 4위(55조원, 9.2%), 중국 5위(39조원, 6.5%)에 이어 한국이 6위(20조원, 3.3%)로 글로벌 반도체 가치사슬 참여 주요국 중 최하위를 기록했다.

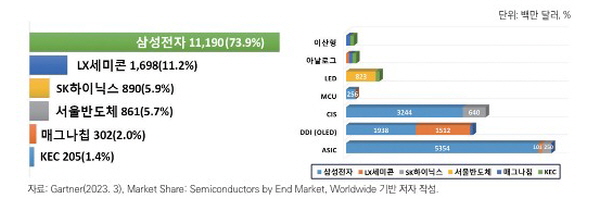

이중 지난해 한국의 비메모리(자체 및 파운드리 위탁 생산 물량 합산) 반도체 매출 총액은 151억달러(약 20조원)로 이중 삼성전자가 112억달러(약 15조원, 73.9%)로 1위, LX세미콘이 17억달러(약 2.2조원, 11.2%)로 2위, SK하이닉스가 8.9억달러(약 1.2조원, 5.9%)로 3위를 기록해 상위 3대 대기업 비중이 90% 이상을 차지한 것으로 나타났다.

이들 대기업이 안정적 글로벌 판로를 확보한 스마트폰, 텔레비전 등 ICT 최종재 투입 소자를 제외하고는 세계 비메모리 시장 내 한국의 존재감은 미미하다. 수십 년간의 시스템반도체, 팹리스 산업 지원 정책에도 판로 확보의 지난(至難)함과 높은 세계 시장의 벽을 새삼스레 절감하게 되는 대목이다.

미국은 집적회로는 물론 PC 및 스마트폰의 발원(發源) 국가로서 CPU 및 AP 등 범용 프로세서, 유무선 통신 및 GPU, FPGA 등 시장을 대부분 독점하고 있다.

유럽은 자동차 및 산업용 로봇 등 주력 수요산업 內 임베디드 시스템 관련 소자 즉, MCU, 이산형과 전력제어(PMIC) 및 광학/비광학 센서류에 강점이 있다.

일본은 유럽과 비슷하게 자동차, 정밀 기계 등 특정수요 대상 MCU, 이산형 반도체와, CMOS 이미지센서 및 정밀 통신소자 등 자체·범용 수요가 있는 분야에도 일부 경쟁우위를 보유하고 있다.

대만은 ‘시장형 선택과 집중’ 즉, 스마트폰, 태블릿, PC 등 투입 수요가 큰 일부 소자군에 강점을 지니고 있다.

중국은 폭넓은 제조업 포트폴리오에 기반, 다양한 소자 전반에 걸쳐 기업군을 보유하고 있다.

미중 패권경쟁으로 촉발된 ‘반도체 전쟁’의 시대를 맞아 우리 정부와 기업 역시 비메모리 산업 발전을 목표로 자원 투입 확대를 꾀하고 있다.

경희권 부연구위원은 “많은 재원을 투입하더라도 우리 기업들의 시장 개척 가능성이 낮거나 성공하더라도 단일 소자 시장 규모가 크지 않은 경우 예산 사용의 타당성 및 경제안보 레버리지 확보 목표와의 괴리가 우려된다”며 “한정된 국가 자원의 낭비 예방과 목표 달성을 위한 실체적 대안 모색을 위해서는 시스템반도체 분야의 복합적 다양성과 메모리와의 차별점에 대한 명확한 인식, 그리고 국내 역량의 다각적 실태 파악에 기반한 국가적 전략 수립이 시급하다”고 밝혔다.

수요산업 및 용도별 시스템반도체 소자는 매우 다양하며 개별 기업의 규모, 강점 기술 분야(도메인), 비즈니스 모델 역시 천차만별이다. 제품별로 각 소자의 용도 및 특성, 그리고 경쟁우위 구성요소가 완전히 다른 시장이라고 보아도 무방할 정도다.

경희권 부연구위원과 김상훈 선임연구위원은 한목소리로 “반도체뿐 아니라 모든 분야에서 新수종 사업의 성공률은 높지 않으며, 주요 기업은 물론 국가적으로도 다종(多種) 소자 및 기술을 포괄하는 포트폴리오 접근이 필요하다”고 강조했다.