주요 4개국 PCB 시장은 자동차 전장용, IoT로 성장세로 돌아설 것

팬아웃-웨이퍼레벨패키지 기술 양산적용, 영향 점차 확대

올해 국내 전자회로기판 시장은 6.0% 성장한 9.5조원 규모가 될 것으로 전망됐다.

국내 시장은 생산액을 기준으로 1998년 이후 연평균 10.2%의 성장률을 보이며 2016년에 8조9,600억원 규모까지 성장하였으나 최근 3년간 연속 마이너스를 기록한 바 있다. 세계 전자회로기판(PCB) 시장은 2020년까지 약 3%대 성장률을 기록할 것으로 보인다.

한국전자회로산업협회가 발간한 전자회로기판 산업협황 보고서에 따르면, 세계 전자회로기판 생산의 81.6%를 차지하는 4개국(한국, 중국, 일본, 대만)의 성장률이 주춤한 것으로 나타났다. 스마트폰과 컴퓨터 관련 시장의 침체와 수요보다 공급이 앞서 가격이 떨어졌다. 반면 올해는 자동차 전장용, IoT 시장의 성장과 스마트폰의 상향 평준화에 따라 연평균 성장률(CAGR) 2.8%가 될 것으로 내다 봤다.

경연성 PCB (출처: 삼성전기 홈페이지)

대만과 일본은 해외 생산이 자국 내 생산을 초과했고, 우리나라는 올해부터 해외 생산 비중을 늘릴 것으로 보인다. 그 중에서도 베트남에서의 생산비중이 높아질 전망이다.

제품별 기판 생산(2016년)을 보면 경성(Rigid) 기판 51%, 연성 (Flexible)기판 20.3%, HDI 기판 14.4%, IC-Substrate 14.3%를 차지했으며 경성기판 중에서는 4층~6층 기판이 전체의 23.9%를 차지했다. 팬아웃-웨이퍼레벨패키지(FO-WLP) 기술이 양산 적용되면서 스마트폰용 AP에 사용되던 플립칩-칩스케일패키지(FC-CSP) 기술을 가진 기업들의 실적은 줄어들었다. 2017년 이후에는 점차적으로 FO-WLP 기술의 영향이 확대될 것으로 보았다.

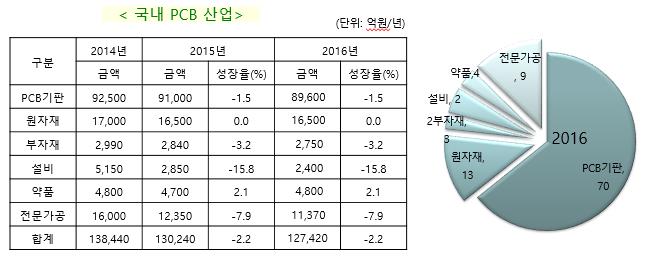

2016년 시장, 전년대비 1.5% 감소한 8조 9,600억원

OLED디스플레이용 FPCB에 채용되면서 성장 예상

2016년 국내 전자회로기판의 생산규모는 전년대비 1.5% 감소한 8조 9,600억원을 기록했다. 프리미엄폰 시장이 정체되면서 둔화되었지만 2017년에는 6.0% 성장한 9조 5,000억원이 예상된다. 국내 스마트폰 제조기업의 신제품 출시와 해외 글로벌 기업의 제품에 OLED 디스플레이용 FPCB에 국내 업체 제품이 채용되기 때문이다. 또, 플렉서블 분야가 재도약 하면서 성장을 주도할 것으로 예상된다.

기판별로는 경성기판(HDI기판 포함) 51.0%, IC-Substrate 26.6%, 연성기판이 22.4% 차지했다. IoT, IoE용 전자기기와 모바일 기기의 다기능, 고기능 실현을 위한 고밀도/미세 패턴 PKG기판, Build-up기판(HDI), 서버, 슈퍼컴퓨터용 고다층 기판 등이 생산을 주도할 것으로 보인다. 경성기판은 0.7% 성장해 4조 6,000억 규모로 예상되고 연성기판은 역성장을 멈추고 24.4%의 큰 폭으로 성장해 2조 5,000억원으로 예상된다. PKG기판은 FC-CSP실적에 따라 유동적일 것으로 보여 0.8%성장해 2조 4,000억원으로 전망된다.

원자재, 전년대비 0.6% 감소한 16,400억원

연성기판용 소재 수요증가로 회복될 것

2016년 후방산업 중에서 원자재는 전년대비 0.6% 감소해 1조 6,400억원이었다. 특히 연성기판용 소재가 2.0%로 감소하였으나 감소폭은 줄어들었다. 2017년에는 연성기판용 소재 수요증가에 힘입어 1조 7,550억원 규모로 회복될 것으로 보이고, 경성기판용은 전년과 비슷한 10,600억원 규모로 예상된다. 동박은 수요가 정체되고 가격이 떨어지면서 생산비중을 줄이고, 부가가치가 높은 전장용 동박의 생산비중이 높아지면서 수급불균형이 초래되었는데 작년에 이어 올해도 이어질 전망이다.

국내 PCB 산업 (출처: KPCA)

부자재 생산액은 전년대비 1.4% 감소한 2,800억원을 기록한 가운데, Solder Resist(PSR)가 900억원 규모로 32.1%를 차지하고 있다. 올해는 작년보다 5.7% 증가한 2,960억원 규모로 예상되고 PSR은 950억원 규모가 될 것으로 봤다. Bit 생산은 제조 기술력이 평준화 되면서 가격 경쟁력이 높은 중화권에 밀리고 있다. CNC Drill Bit 와 Router Bit는 전년과 같은 실적을 보일 것이며 Dry film은 6.7% 증가한 1,120억원 규모를 나타낼 것으로 예상된다.

약품 생산은 3.2% 감소한 34,550억 규모로 금도금과 동도금 약품이 전체의 62.6%를 차지한다. 올해는 금도금이 3.9%, 동도금이 5.9%로 전체 시장은 4.8% 성장해 4,770억원 규모로 보고 있다. 금도금과 동도금은 시장 점유율을 높여가고 있으나 필동도금이나 PKG용 약품 등 고부가가치 약품은 아직 해외 업체들이 시장을 장악하고 있는 상황이다.

약품 생산 국산화로 원가 절감, 후발업체 진입 기회 생겨

산업현황 보고서에 따르면 “약품에 대한 최종 소비자의 승인문제와 신뢰성 확보를 위한 양산 라인에서의 테스트가 필요해 후발 업체들이 시장에 진입하기가 어렵다”며 “최근에는 국내 기판제조업체들과 협력을 통해 국산화함으로써 원가 절감을 하고 있어 참여 기회가 생기고 있다”고 전했다.

설비 시장은 도금/표면처리 공정용 설비가 28.6% 감소하면서 전년대비 15.8% 감소한 2,400억 규모를 보였다. 올해도 신규투자는 최소화할 것으로 보이나 연성기판용 신규 투자 수요와 해외 공장, 합리화 부분에서의 투자는 계속될 것으로 예상된다.

보고서는 “국내 수요는 많이 줄었지만, 기술력을 바탕으로 중화권에 진출했고 동남아시아로도 진출하면서 글로벌 경쟁력을 강화시키고 있다”고 설명했다.