기사입력 2021.06.08 14:02

■ 2021년 하반기, 수요·가격 지속 증가

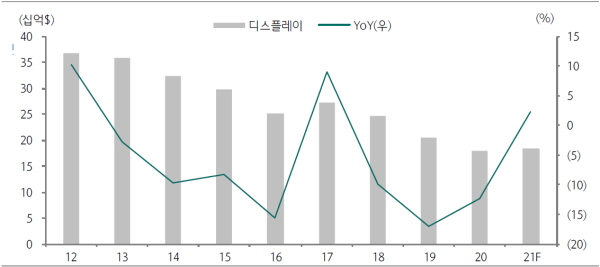

2010년 들어 디스플레이 수출은 2012년과 2017년을 제외하고 매년 역성장했다. 연간 디스플레이 수출은 2012년 369억달러로 최고치를 기록한 이후에 2020년 180억달러로 감소했다. 8년간 51%가 감소했다. 최근 3년간 디스플레이 수출 연평균 증감률 역시 2018년 -10%, 2019년 -17%, 2020년 -12%로 지속 역성장했다.

이러한 추세는 2020년 하반기 들어 반등하기 시작했다. 2020년 상반기 코로나19 수요감소로 인해 글로벌 LCD TV 판매량은 9,100만대로 2019년 상반기 대비 7.3% 감소했으나 2020년 하반기 미국 등 선진국들이 각종 보조금을 확대했고, 소비자들의 여가시간이 증가하며, 2020년 3분기 LCD TV 판매량은 6,193만대로 2020년 2분기 4,506만대 대비 37.4% 급증하면서 LCD TV 패널 가격이 반등하기 시작했다. 32인치 LCD TV 오픈셀 가격은 2020년 5월 33달러에서 2021년 5월 88달러로 167% 급등했다. 이는 LCD 역사상 가장 높은 가격 상승세다.

▲한국 디스플레이 수출 추이 및 전망(자료 : 하나금융투자)

OLED TV도 수요가 지속 증가하고 있다.

전체 디스플레이 수출과 달리 OLED 수출은 2012년 46억달러, 2016년 69억달러, 2020년 109억달러로 8년간 137% 성장했다. 디스플레이 수출 중 OLED 비중도 2012년 12%, 2016년 27%, 2020년 61%로 상승했다.

특히 이런 추세에 발 맞춰 2021년 1분기 OLED 출하량은 지속 증가 중이다. 유비리서치에 따르면 2021년 1분기 소형 OLED 출하량은 1억4,000만대로 전기대비 135.5% 감소했지만, 전년동기대비 32.4% 증가했다. 중대형 OLED 1분기 매출액은 14억6,000만달러로 전기대비 16.9%, 전년동기대비 156.3% 증가했다. TV용 OLED 패널 판매량은 역대 최대인 160만대를 기록했다.

이와 같은 가파른 성장률은 모바일 시장 내 OLED 침투율 상승, OLED TV 시장 확대, 노트북 등 신규 OLED 수요처 확대, 중국 패널 메이커 가동률 상승 등에 기인하는 것으로 분석된다.

■ LCD 패널 공급 부족, 3Q 가격 상승·4Q 가격 둔화

지난 2020년 7월부터 LCD 패널 가격은 TV 수요, 재택 근무 및 온라인 교육 활성화로 인해 IT 패널 수요가 증가하며 지속 상승 중이다. 2021년 5월 말 기준으로 55인치 글로벌 LCD 패널 가격은 223달러로 전년동기대비 117% 상승했다.

지난해 하반기에는 DDI에 이어 유리기판 공급 부족이 심화되고, 올해 초부터 TV/IT 수요 강세 지속과 DDI 공급 부족이 심화되며, LCD 패널 가격은 강세가 지속되고 있다.

이런 추세는 올해 하반기에도 지속돼 2021년 연평균 LCD 캐파는 9% 증가하나 DDI, 유리기판, PMIC 등의 주요 부품 공급 부족 이슈는 지속 될 것으로 보인다.

특히 중국 LCD 업체들은 국내 업체들의 LCD 라인 폐쇄 이후 수익성 확보로 집중하는 전략으로 우회하고 있다.

LCD 1위 업체인 중국 BOE는 6월부터 3개월간 LCD 정기 보수에 돌입할 예정으로 BOE의 2021년 3분기 LCD 패널 생산량은 일정 수준 감소할 것으로 예상된다. 대만 AUO도 2021년 2분기에 일부 라인의 정기 보수를 시행했다.

이에 LCD 가격은 2021년 3분기까지 가격 상승세가 지속될 것으로 보인다.

반면에 중대형 DDI 공급 부족이 완화되고, 코닝이 우한 10.5세대 신규 유리기판 공장 램프업을 시작하며, 9월부터 광저우 신규 공장 가동이 예정돼 있어 2021년 4분기에는 전분기 대비 소폭의 하락이 예상되고 있다.

■ 디스플레이 시장 OLED 성장 본격화

올해 하반기 디스플레이 시장은 OLED가 주도할 것으로 예상된다.

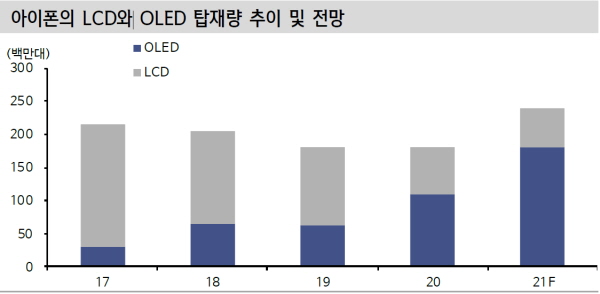

올해 아이폰 13 4개 모델 모두에 OLED 탑재가 전망되고 있으며, 대부분 OLED를 탑재하는 5G 스마트폰의 출하량이 6억1,000만대로 전년대비 125.9% 증가하며, 올해 스마트폰용 OLED 패널 수요는 7억5,000만대로 전년대비 46.2% 증가할 것으로 전망된다.

▲아이폰의 LCD와 OLED 탑재 추이 및 전망(자료 : 신한금융투자)

또한 삼성의 OLED 노트북, 2022년 애플의 아이패드 OLED 탑재 등도 플러스 요인이다.

2021년 4월 삼성전자는 OLED를 탑재한 ‘갤럭시북 프로’ 노트북을 공개했는데 2021년 삼성디스플레이는 13.3형부터 16형까지 노트북용 OLED 라인업을 10종 이상으로 확대함으로써 본격적으로 노트북용 OLED 패널 생산을 확대할 예정이다. 노트북용 OLED 패널 생산량은 2019년대 1만2,000대, 2020년 16만5,000대, 2021년 100만대로 매년 큰 폭으로 성장할 전망이다.

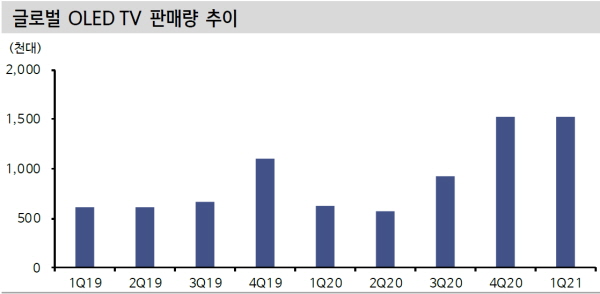

▲글로벌 OLED TV 판매량 추이(자료 : omdia, 신한금융투자)

이런 가운데 삼성전자 TV의 OLED 출시가 관심을 모으고 있다. 세계 TV 시장 1위인 삼성전자지만 OLED TV는 출시하지 않고 있다. 현재 OLED TV 판매사는 약 16개로 판매량 기준 점유율은 LG 전자 56%, 소니 22%, 파나소닉 9%를 점유 중이다.

최근 시장 분위기에 따르면 삼성전자 또한 OLED TV 시장 참여를 고려중으로 프리미엄 시장 내 입지 강화를 위해 삼성전자의 OLED TV 시장 참여는 가능성이 높을 것으로 분석된다.

특히 삼성전자는 삼성디스플레이와 함께 2022년에 QD-OLED TV를 출시할 것으로 알려진 바 있는데 이를 위해 삼성디스플레이가 2021년 4분기부터 월 2만5천장 규모로 첫 번째 Q1 양산 가동을 시작할 것으로 알려지고 있다. 다만 삼성디스플레이의 공간 부족 등을 이유로 추가 증설은 어려울 것으로 보이며, 2022년, 2023년에도 Q1 라인만을 통해 생산 가능한 OLED TV 패널은 약 100만대에 그칠 것으로 추정되고 있다.

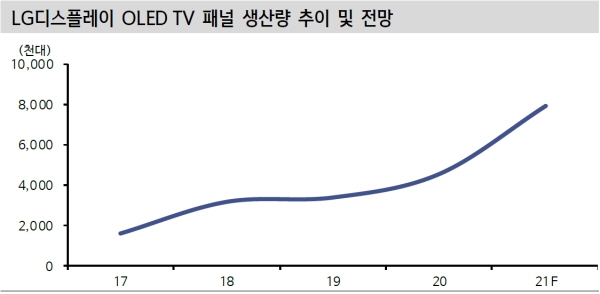

이런 가운데 LG 디스플레이의 경우 2021년 중국 광저우 OLED TV 라인이 풀가동하면서 2021년 3분기 영업이익이 흑자 전환할 것으로 전망되고 있다.

▲LG디스플레이 OLED TV 패널 생산량 추이 및 전망(자료 : omdia, 신한금융투자)

2022년 LG디스플레이의 OLED TV 패널 생산량은 약 1,000만대 수준으로 올라가면서 구조적인 영업이익 흑자가 유지될 것으로 예상되고 있다.

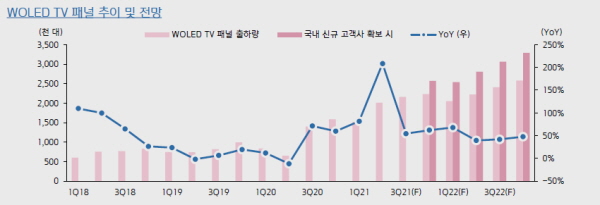

현재 LG디스플레이의 WOLED TV 패널 캐파는 월 약 15만장으로 약 800∼1,000만대 생산이 가능하다. 특히 WOLED TV 패널 시장 진입을 위해서는 대형 패널의 Oxide TFT 기술 안정화가 선행돼야 하며, BOE는 최근 CEC Panda 인수를 통해 대형 패널용 Oxide TFT 기술을 개발할 계획으로 알려져 있다. BOE 등 중국 업체들의 WOLED TV 패널 시장 진입은 2025년 이후로 예상된다.

▲WOLED TV 패널 추이 및 전망(자료 : 키움증권)

LG디스플레이의 POLED 캐파는 현재 월 4만5,000장 규모로 경쟁사 대비 적은 수준이다. 이에 북미 고객사향 출하 확대 및 POKED IT 패널 공급을 위해 2021년 4월 월1만5,000장 증설이 예상되며, 2022년 2분기부터 가동이 시작될 것으로 전해지고 있다.

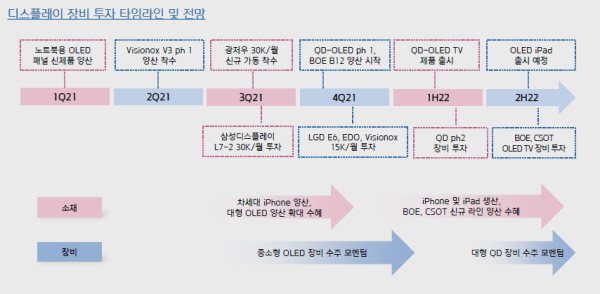

BOE, CSOT 등 중국 패널 업체들은 모두 연내 신규 투자 보다는 장비 셋업 및 수율 안정화에 집중할 것으로 알려지고 있다. 2022년 2분기 OLED TV 패널 투자 가능성이 있으나 양산은 최고 2025년 이후로 예상되고 있다.

▲디스플레이 장비 투자 타임라인 및 전망(자료 : 키움증권)

■ 中 시장 지배력 강화

중국의 LCD 시장 지배력은 지속 강화될 것으로 전망된다.

중국의 LCD 생산능력 규모가 경쟁 국가(한국, 대만, 일본)를 이미 크게 앞지른 가운데, 신규 LCD 증설은 중국에서만 진행되고 있는 상황이기 때문이다.

이에 앞으로 중국산 LCD 사용은 크게 확대될 것으로 예상되며, 실제 한국 세트(TV 기준) 업체들의 중국산 LCD 패널 채용 비중은 지속 상승 중인 것으로 파악되고 있다.

중소형 OLED 패널 시장도 경쟁이 심화되고 있다. 현재 중국 BOE와 Visionox는 OLED 패널(스마트폰용 기준)을 중국외 세트 업체에 공급 중이다. 특히 BOE는 애플향 OLED 패널 공급을 위해 B12 설비에서 LTPO 투자를 진행 중인 것으로 알려지고 있다.

주요 중국 업체들의 연간 OLED 패널 출하량은 2019년 32만4,000대에서 2020년 51만2,000대, 2021년 91만5,000대로 증가할 것으로 전망되고 있다.

.jpg)

▲삼성디스플레이와 LG디스플레이 7세대, 8.5세대 중대형 캐파 현황 및 전망(자료 : omdia, 하이투자증권)

2021년 4월 정보통신기술(ICT) 수출은 170억6,000만달러로 전년동월대비 32.6% 증가했고, 수입은 107억8,000만달러로 전년동월대비 21.5% 증가했다. 무역수지는 62억9,000만달러의 흑자로 잠정 집계됐다.

2021-05-20 오후 4:03:50by 배종인 기자

5월 반도체 수출이 100억달러를 넘어서며, 반도체 수출이 11개월 연속 증가했다. 이러한 수출 실적은 스마트폰 5G 본격화, 데이터센터 업체들의 투자 확대 등으로 모바일 및 서버용 메모리 주문 확대가 본격화되면서, 응용처별 수요 확대로 인한 메모리 고정가격 상승, 비대면 경제 수요 지속에 따른 노트북 판매 호조 등이 원인으로 분석된다.

2021-06-02 오후 4:26:06by 배종인 기자

.jpg)

삼성 Neo QLED가 업계 최초로 독일 인증기관 VDE(Verband Deutscher Elektrotechniker)의 ‘공간 최적화 사운드(Spatial Sound Optimization)’ 기술을 인증 받으며, 소비자들에게 최적의 음향 환경을 갖춘 시청 환경을 제공하는 성능을 인정받았다.

2021-06-08 오전 8:32:47by 명세환 기자

[열린보도원칙] 당 매체는 독자와 취재원 등 뉴스이용자의 권리 보장을 위해 반론이나 정정보도, 추후보도를 요청할 수 있는 창구를 열어두고 있음을 알려드립니다.

고충처리인 장은성 070-4699-5321 , news@e4ds.com