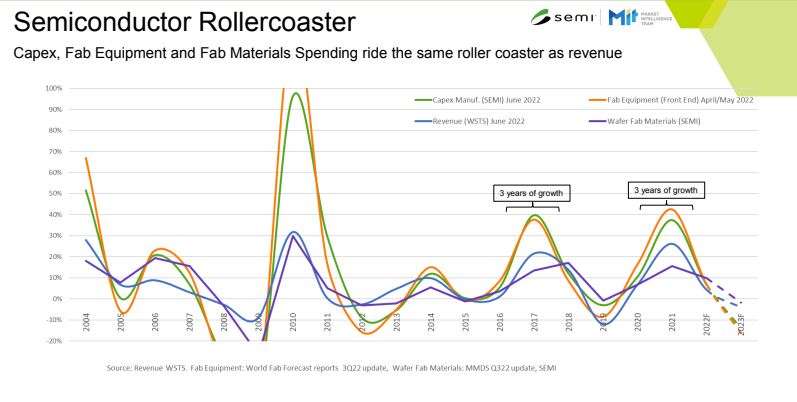

반도체 산업은 롤러코스터처럼 상승·하락의 주기성을 띄고 있다. 2023년 반도체 전망은 한 목소리로 다운사이클을 외치고 있는 가운데 세미콘 코리아 2023에서 팹과 소부장 산업에 대한 전망을 밝혔다.

평균 7% 역성장, 소부장 덩달아 위축

“2024년 업황 회복의 해, 17.5% 증가”

▲반도체 시장의 주기성(자료:SEMI)

반도체 산업은 롤러코스터처럼 상승·하락의 주기성을 띄고 있다. 2023년 반도체 전망은 한 목소리로 다운사이클을 외치고 있는 가운데 세미콘 코리아 2023에서 팹과 소부장 산업에 대한 전망을 밝혔다.

3일 국제반도체장비재료협회(SEMI)가 주최한 국내 최대 반도체 산업 전시회 세미콘 코리아 2023을 개최하며 미디어 브리핑이 진행됐다. 이날 SEMI의 이나 스크보르초바(Inna Skvortsova) 마켓 리서치 애널리스트가 거시경제와 반도체업계 전망에 대해 발표했다.

스크보르초바 애널리스트는 “2023년 반도체 시장 전망은 전년대비 550억달러 하락한 마이너스 7%의 역성장을 평균으로 예상하고 있다”며 “극단적인 전망에선 22% 하락을 예측하는 조사기관도 있으나 보수적인 접근에서는 옴디아, 가트너, IC인사이츠 등에서 0.2%∼5.8%까지로 내다보고 있다”고 말했다.

.jpg)

▲이나 스크보르초바(Inna Skvortsova) SEMI 마켓 리서치 애널리스트가 세미콘 코리아 2023서 미디어 브리핑을 진행하는 모습

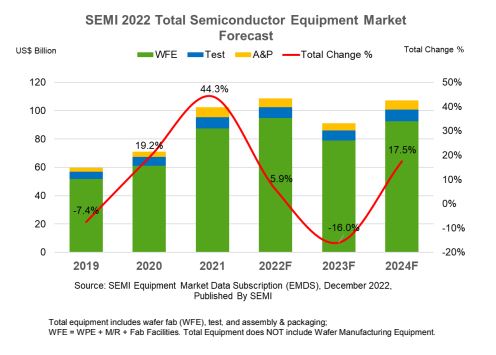

반도체 산업 눌림목이 현실이 된 가운데 장비 시장도 덩달아 하락할 것으로 예측된다. SEMI 반도체 장비시장 전망에 따르면 전체 반도체 장비 시장은 2022년 5.9% 성장한 1085억달러를 기록했으나 2023년은 16% 하락한 912억달러로 떨어질 것으로 보인다.

장비 시장에서 가장 높은 비중을 차지하는 웨이퍼 팹 장비(WFE)는 2022년 8% 성장율을 뒤로 하고 2023년 17%가 하락한 788억달러로 전망된다. 세부적으론 WFE 시장에서 55% 이상을 차지할 것으로 전망되는 파운드리 및 로직 부문에서 9% 감소, D램이 지난해 10% 감소에 이어 올해도 23% 하락이 예상되며, 낸드도 2022년과 2023년 각각 4%, 36% 하락이 전망된다고 밝혔다.

더불어 테스트 및 어셈블리·패키지 시장도 각각 7.3%와 13% 감소가 예상되며 지난해 이어 2년 연속 하락세를 기록할 전망이다. 특히 어셈블리·패키지는 지난해 15% 하락에 이어 올해 13%나 더 떨어지며 불확실한 시장 상황과 경제 전망이 크게 반영된 것으로 풀이했다.

소재 시장도 마찬가지로 올해 6% 감소해 412억달러로 내려앉을 것으로 예측된다. 지난해 150억 달러를 넘어선 실리콘 웨이퍼 매출은 142억달러로 떨어지며 하락세를 보였다.

▲SEMI 2022 전체 반도체 장비 시장 전망(자료:SEMI)

눌림목이 있으면 오름세가 기다리는 법이다. SEMI는 2024년을 업황 회복의 해로 내다봤다. 반도체 장비 시장은 2024년 17.5% 상승한 1072억달러로 시장 회복과 함께 성장이 재개될 것으로 내다봤다. △소재 △어셈블리 △패키징 △테스트 등 반도체 공급망 전체에서 업황 회복이 예상되고 있다.

스크보르초바 애널리스트는 “전세계적으로 84개 새로운 팹이 구축되고 있으며 특히 미국이 최근 3년간 18개의 팹을 착공해 이전 3년과 비교했을 때 15개 이상 증가했다”며 각 국가별 반도체법과 대 중국 수출규제 강화 추세로 자국 내 반도체 투자가 더욱 가속화될 것으로 예상했다. 이러한 추세 속에서 그는 “아시아 일부 국가에 팹이 집중될 것으로 본다”고 언급했다.

전체 반도체 케파는 지속적으로 증가하고 있는 가운데 아시아 국가 중에서 대만이 현 시점 반도체 소재를 가장 많이 소화하는 시장이다. 그 다음 한국이 위치해 있으며 일본 아래에 있던 중국이 향후 3번째 시장으로 올라올 것으로 예상된다.