2022년에 역성장을 보였던 디스플레이 시장이 2023년에 면적기반 수요 회복을 바탕으로 2024년부터 새로운 수요를 바탕으로 성장할 수 있을 것이라는 전망이 제시됐다.

▲데이비드 시예(David Hsieh) 옴디아 수석 연구 이사가 ‘2023년 디스플레이 산업 10대 토픽 전망’을 주제로 기조연설을 하고 있다.

옴디아, 2023년 상반기 디스플레이 컨퍼런스 개최

대형 면적 시장 변모, LCD 투자無 장기적 공급부족

2022년에 역성장을 보였던 디스플레이 시장이 2023년에 면적기반 수요 회복을 바탕으로 2024년부터 새로운 수요를 바탕으로 성장할 수 있을 것이라는 전망이 제시됐다.

옴디아(OMDIA)는 3월15일부터 16일까지 ‘2023년 상반기 한국 디스플레이 컨퍼런스’를 개최했다.

이틀간 전세계 옴디아 소속 디스플레이 연구원이 전 세계 디스플레이 산업 동향 및 시장 전망을 공유하는 이번 행사에서는 2023년 디스플레이 산업 10대 토픽 전망 및 대형 디스플레이 산업 전망, 중장기 디스플레이 시장 최신 전망 등 디스플레이 산업 10대 주제와 산업용 디스플레이 시장, 활용 사례들이 다뤄졌다.

첫째 날 첫 번째 발표를 담당한 데이비드 시예(David Hsieh) 옴디아 수석 연구 이사는 ‘2023년 디스플레이 산업 10대 토픽 전망’을 주제로 기조연설을 진행했다.

데이비드 시예는 2022년은 디스플레이 역사상 처음으로 출하면적이 줄어드는 어려움을 겪었다고 밝혔다.

출하면적은 2022년에 2억4,976만㎡로 전년대비 4% 감소했는데, 2023년에는 2억6,017만㎡전년대비 4% 증가하고, 2024년에 전년대비 7% 증가해 2억7,900만㎡가 될 것으로 전망됐다.

특히 대형 면적 주도의 시장으로 바뀌고 있는데, 코로나 기간 동안 TV, 모니터 등 셋트 제품의 판매가 감소함에도 불구하고 판매량 대비 면적은 증가했는데, 이는 소비자의 행동 패턴이 대형화면을 지지하는 것으로 바뀐 것으로 분석됐다.

이에 패널 메이커들이 소형화면을 줄이고, 대형화면으로 전환하는 전략 수립에 들어가고 있으며, TV 수요가 좋지 않다는 사실을 세트 판매 대수가 아니라 면적으로 다시 들여다봐야 한다고 언급했다.

특히 이러한 행동 패턴은 가격에 따라서도 나타나는데 소형과 대형의 가격차이가 큰 차이가 없어 소비자들의 TV 쇼핑 행태가 대형으로 옮겨가는 원인이 된다고 분석했다.

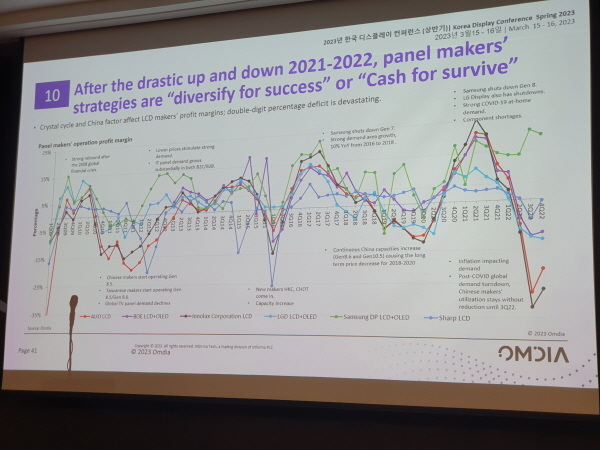

공급과 관련해서는 과잉공급이 없어졌는데 이는 패널메이커가 생산을 줄이고, 지금 현재 패널을 생산하면 할수록 손해가 발생하기 때문이라고 밝혔다. 이런 가운데 중국에서 새로운 공장 건설을 유보하고 있고, 일부메이커들이 LCD 생산을 포기하면서 장기적으로는 공급부족 현상이 발생할 수도 있다고 지적했다.

특히 중국TV 업체들이 한국이나 일본 기업과는 다르게 패널 구입에 적극 나서고 있는데 이는 지금 현재 상황이 패널 가격이 가장 싸다고 생각하는 것으로 판단해 물량을 확보하고, 가격 상승에 대비 또는 가격 상승시 내다 팔기 위한 행태로 볼 수 있고, LCD 패널 대부분을 중국에서 생산하고 있기 때문에 중국 업체들이 가격 상승을 원하기 때문에 이런 현상들이 발생하고 있다고 전했다.

투자와 관련해서는 2022년에 LCD 팹 신규 건설은 없었으며, IT나 OLED 중심으로 투자가 진행된 것으로 전해졌다.

최근 디스플레이업체들의 경우 차량용 디스플레이, 키오스크, 휴먼 머신 인터페이스 등 신규 산업용디스플레이 수요 발굴에 적극 나서고 있는 것으로 나타났다.

특히 대만 업체들이 이 수요 발굴에 적극 나서고 있는데, 이는 대만 생산 시설이 대부분 20년이 넘은 6세대 시설로 이 장비를 운용할 수 있는 시장으로 산업용 수요 등의 니치마켓을 타깃으로 하고 있는 것으로 나타났다.

8.5세대 업체들의 경우 산업용 수요는 패널을 커팅하는 커스터마이징 또는 새로운 포토마스크 기술로 패널을 나눠 생산하는 방안이 제시됐다.

대형 면적과 관련해서는 평균 사이즈가 55인치 이상으로 분석됐고, 60인치 이상의 경우 소비자들은 첨단 기술이 들어가는 제품을 찾는 것으로 나타났다.

코로나19 이후 사람들이 IT에 의존하면서 새로운 모양의 제품 개발 요구가 높아지고 있는데 이에 따라 커브드 제품, 고주파 제품, 미니LED, OLED의 수요가 성장한 것으로 나타났다.

특히 중국의 경우 8.5세대 디스플레이를 70개로 커팅한 15.3인치 제품 등을 출시하고 있는데 이는 중국 내수를 바탕으로 새로운 시장을 창출하려는 시도로 분석됐다.

모바일 OLED와 관련해서는 현재 한국 제품의 점유율이 높이만 중국 스마트폰 업체들을 중심으로 중국 로컬 OLED 채용이 늘어나고 있어 중국의 시장 점유율이 높아질 것으로 예상됐다.

다만 폴더블 또는 롤러블 제품의 경우 아직 중국의 기술력이 못 미치는 만큼 중국이 이 시장에 들어오기까지는 상당한 시간이 걸릴 것으로 예상됐다.

오토모티브 시장과 관련해서는 전기차의 등장으로 수요가 증가하고 있는데 소비전력이 중요하고, 명암비를 높인 제품이 자동차 등 오토모티브 시장에서 중요한 요소로 평가되고 있다.

특히 이 분야는 폼팩터 및 사이즈가 다양하고, 이머징 등 다양한 컨셉이 있는 것이 특징이다.

데이비드 시예는 마지막으로 2022년 불황을 겪으며, 디스플레이 업체들의 전략이 ‘성공을 위한 다양화’ 또는 ‘생존을 위한 자금 확보’ 두 가지 경향으로 나눠지고 있다며, 살아남기 위해서 회사에 가장 중요한 것은 매출이라고 조언했다.

.jpg)