8인치 반도체, 높아지는 위상...호실적에 설비투자 확대

기사입력 2022.04.13 10:09

2024년 생산량 21%↑, 月웨이퍼 120만장↑

지난해 53억달러, 올해 49억달러 설비투자

SK·DB, 8인치 수익성 개선으로 실적 호황

SK·DB, 8인치 수익성 개선으로 실적 호황

코로나19 이후 반도체 수요가 급증하며 8인치(200mm) 파운드리의 몸값이 점점 높아지고 있다. 이에 관련 업계에서 생산라인을 풀가동해 생산량을 늘리고 있으며 설비투자에도 적극적인 움직임을 보이고 있다.

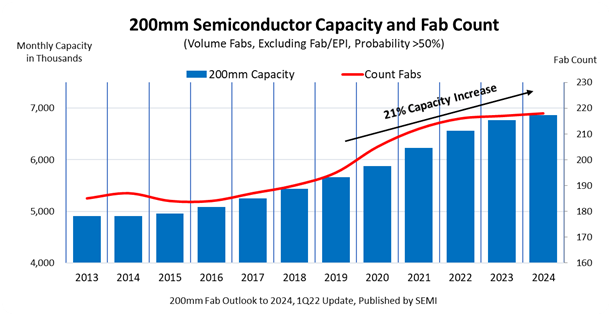

▲8인치(200mm) 반도체 생산 시설 수 및 생산량 (2013 - 2024) *자료 - SEMI

국제반도체장비재료협회 SEMI에서 발표한 최신 200mm 팹 전망 보고서(200mm Fab Outlook)에 따르면 전세계 8인치 반도체 파운드리의 월간 웨이퍼 생산량이 2020년 초와 비교해 2024년 말에 21% 증가한 690만장으로 확장될 것이라고 전망했다.

이는 약 120만장이 증가한 수치로 전세계적인 반도체 수요 증가로 지난해부터 8인치 파운드리 생산량이 급격히 증가한 것이 올해까지 이어지고 있는 상황이다. 업계는 현재 전세계가 겪고 있는 반도체 부족 사태를 극복하기 위해 작년 8인치 파운드리 장비 부문에 53억 달러의 투자를 진행했으며, 올해는 49억달러로 여전히 높은 투자 규모를 유지할 것으로 보인다고 설명했다.

8인치 파운드리가 호황을 맞이하며 SK하이닉스, DB하이텍 등에서 미소를 짓고 있다. 다소 구식공정이라 취급받던 8인치 공정에서 수급이슈가 장기화되며 DB하이텍은 실적이 고공행진하고 있다. DB하이텍의 지난해 연간 매출은 1조원을 처음으로 돌파했으며 생산라인을 풀가동 중이라고 밝힌 바 있다.

SK하이닉스의 자회사 SK하이닉스 시스템IC는 지난해 매출액이 7천억원에 근접하며 전년대비 순이익은 2배 가까이 늘었다. 생산라인을 이전하는 상황에서 일부 라인 가동이 중단되며 매출은 전년대비 소폭 줄었지만 8인치 파운드리 수익성이 크게 개선되며 순이익이 큰 폭으로 늘어났다고 업계는 평가했다.

SEMI는 “올해는 파운드리 분야가 전체 생산량의 50% 이상을 차지할 것”이며 “아날로그분야가 19%, 디스크리트 및 전력 반도체가 12%로 뒤를 이을 것”으로 전망했다. 지역적으로는 중국지역이 2022년에 21%의 점유할 것으로 내다봤으며, 일본이 16%, 대만·유럽·중동지역이 각각 15%를 차지할 것으로 예상했다.

8인치 반도체 장비에 대한 투자는 2023년에도 30억 달러를 넘어설 것으로 전망했다. 파운드리가 전체 투자액의 54%, 디스크리트 및 전력 반도체가 20%, 아날로그 반도체가 19%의 차지할 것으로 보고서는 설명했다.

반면 업계에서는 8인치 생산 증설이 그리 쉽지만은 않을 것으로 내다봤다. 8인치 공정이 구식 취급을 받으며 12인치 공정으로 넘어가는 동안 장비사들이 8인치 시장에서 철수해 수요에 즉각 대응한 증설이 어렵다는 것이다. 지난해 중국 반도체 업체들이 8인치 중고장비를 싹쓸이하며 관련 장비에 품귀현상을 여실히 증명하기도 했다.

이에 SK하이닉스는 8인치 반도체 위탁생산업체인 키파운드리의 인수를 추진하며 월 8인치 생산능력을 8~9만장 상승시킬 것으로 전망했다. 관련 기업들도 설비투자에 적극적인 행보를 보이며 증설 전략을 개별화하고 있다.

SEMI의 CEO인 아짓 마노차는 "5G, 자율주행,IoT, 아날로그 및 전력 반도체 등에 대한 수요가 계속 증가하면서 앞으로 5년 동안 약 25개의 새로운 8인치 생산 라인이 추가될 것”이라고 예상했다.

관련뉴스

-

8인치 웨이퍼 팹 생산량 증가세, 꾸준히 이어진다

SEMI의 최신 200mm 팹 전망 보고서에 따르면, 월간 8인치 팹 생산량이 2020년부터 2024년까지 17% 성장, 웨이퍼 약 660만 장 생산에 이를 것으로 전망했다. 또한, 2024년까지 5G, IoT 장치에 대한 수요를 맞추기 위해 전력 및 아날로그 반도체, MOSFET, MCU, 센서 등을 생산하는 200mm 팹이 22개 신규 건설될 것으로 보인다.

2021-05-26 오전 9:11:26by 이수민 기자

-

SEMI, “2022년 팹 투자 韓 1위”

2022년 전세계 팹 투자 국가 중 한국이 세계 최대 투자 국가가 될 것이라는 전망이 나왔다.

2021-09-17 오전 8:56:40by 배종인 기자

-

SK하이닉스, ‘키파운드리’ 5,758억 인수

SK하이닉스가 8인치 파운드리(Foundry) 기업인 키파운드리 인수를 통해 글로벌 반도체 공급부족을 해결하고 국내 팹리스 생태계 성장에 기여한다.

2021-11-01 오전 10:42:04by 배종인 기자

많이 본 뉴스

[열린보도원칙] 당 매체는 독자와 취재원 등 뉴스이용자의 권리 보장을 위해 반론이나 정정보도, 추후보도를 요청할 수 있는 창구를 열어두고 있음을 알려드립니다.

고충처리인 장은성 070-4699-5321 , news@e4ds.com