기사입력 2025.02.05 09:48

SK하이닉스 주가가 급등하며 K-증시를 이끄는 AI 메모리 대장주로의 입지를 굳히고 있다.

2025-01-06 오후 3:59:27by 권신혁 기자

현재 세계인구는 80억명으로 2050년에는 97억명에 이를 것으로 전망되는 가운데 기후변화로 인해 식량 안보와 농업 생산성이 미래 국가 생존의 큰 챌린지로 급부상하고 있다. 농산업에서의 과학기술, AI, 디지털 전환 등이 핵심 역량 과제로 대두되는 가운데 미래 농업 전망을 논의하기 위해 각계각층 전문가들이 한자리에 모였다.

2025-01-16 오후 4:37:31by 권신혁 기자

가트너(Gartner)가 발표한 2025년 자동차 시장의 주요 트렌드에 따르면 올해 자동차 업계에서는 배기가스 배출에 대한 규제 압박과 서방 국가와 중국 간의 무역 분쟁이 트렌드의 핵심 요인으로 작용할 것으로 전망됐다.

2025-01-20 오후 4:15:47by 배종인 기자

.jpg)

PC 시장이 2023년의 침체를 극복하고 소폭 출하량 회복세를 보이고 있는 것으로 나타났다. 가트너(Gartner)가 지난해 4분기 전세계 PC 출하량이 총 6,440만 대를 기록했다는 예비조사 결과를 22일 발표했다. 이는 전년 동기 대비 1.4% 증가한 수치로, 연간 총 PC 출하량은 2023년 대비 1.3% 증가한 2억 4,540만 대를 기록했다.

2025-01-22 오후 1:21:40by 권신혁 기자

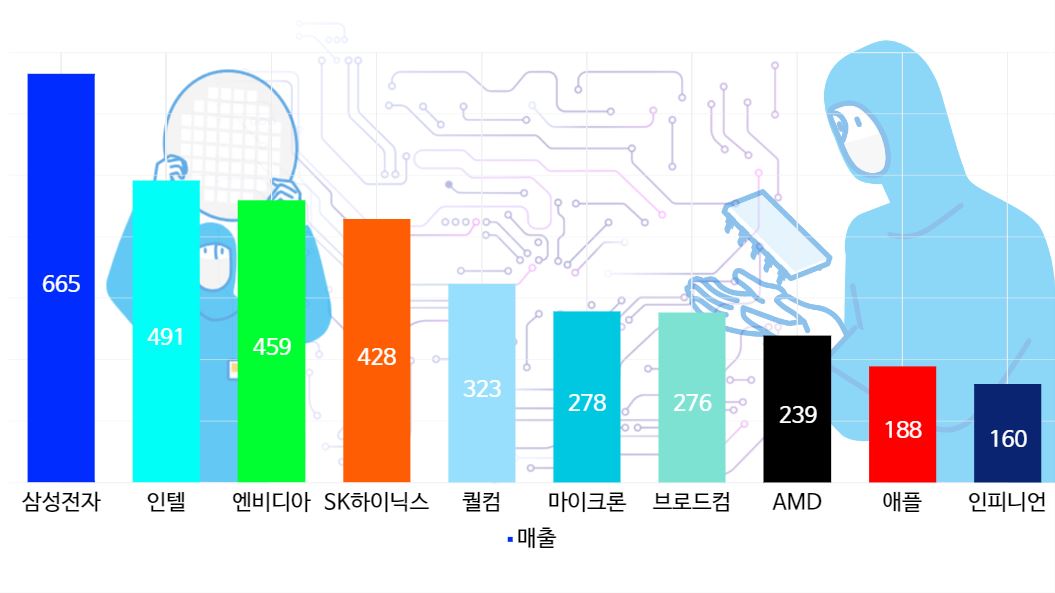

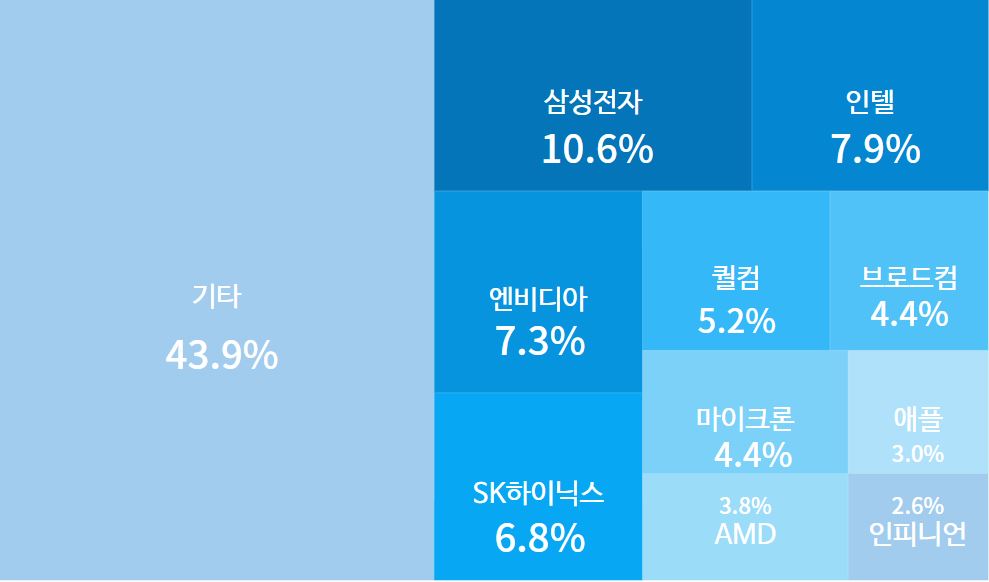

삼성전자가 2024년 연간 실적에서 역대 두 번째인 300조 매출 달성에도 불구하고, 반도체 영업익에서 SK하이닉스에 뒤지며 웃지를 못했다. 삼성전자가 31일 공시한 2024년 4분기 경영실적에 따르면 연결재무제표 기준으로 매출 300조8,709억원으로 기록해 전년대비 16.2% 증가했고, 영업이익은 32조7,260억원을 기록해 전년대비 398.3% 증가했다. 당기순이익은 34조4,514억원을 기록해 전년대비 122.5% 증가했다.

2025-01-31 오전 9:53:08by 배종인 기자

[열린보도원칙] 당 매체는 독자와 취재원 등 뉴스이용자의 권리 보장을 위해 반론이나 정정보도, 추후보도를 요청할 수 있는 창구를 열어두고 있음을 알려드립니다.

고충처리인 장은성 070-4699-5321 , news@e4ds.com